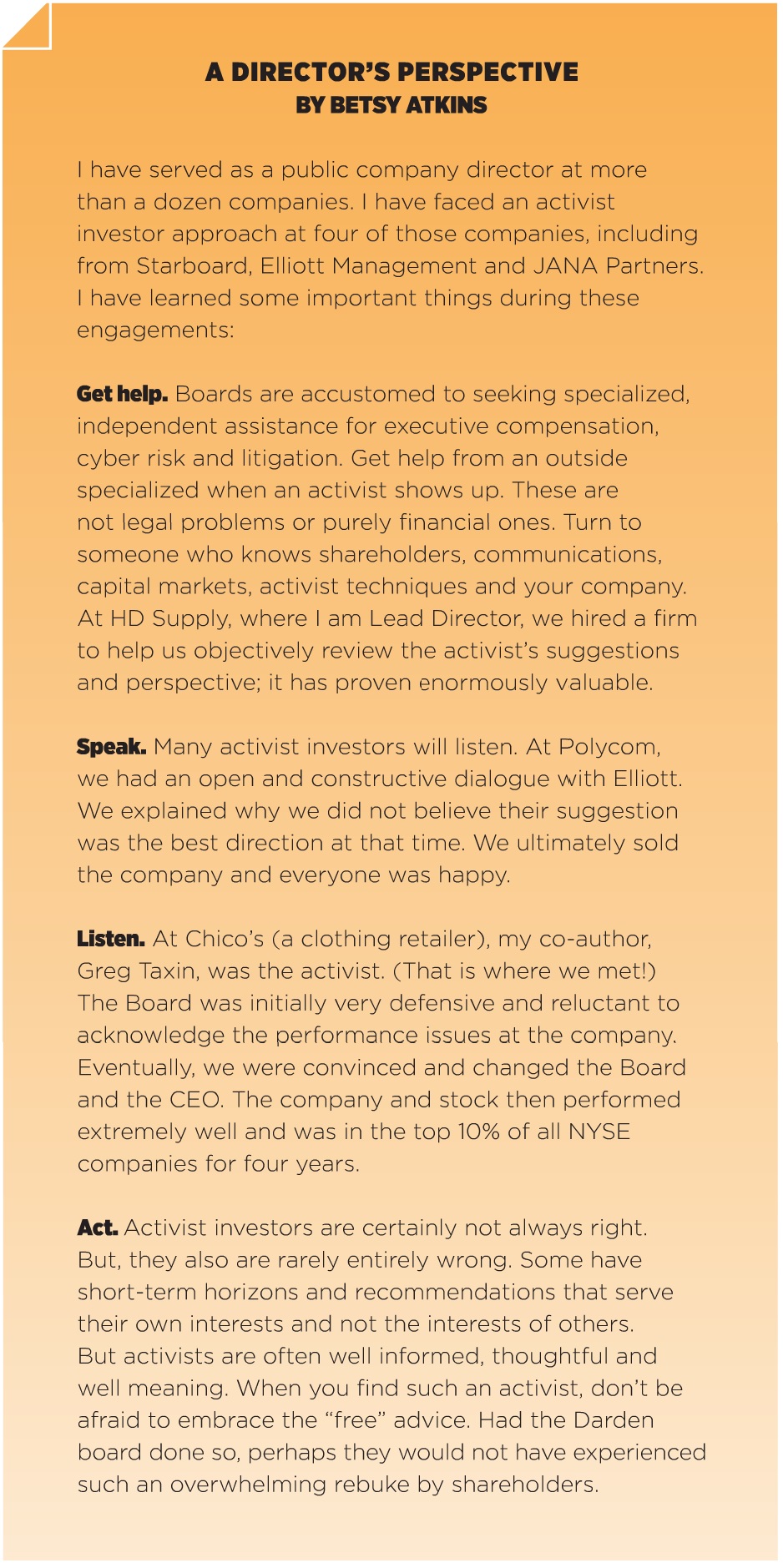

By Gregory Taxin and Betsy Atkins*

Shareholder activism in the U.S. has increased greatly over the past decade, measured not only in scope and the pools of capital dedicated to it but also in sophistication and in the range of tactics employed. There is currently more than $120 billion in dedicated activist funds at work, and these funds launched nearly 300 activist campaigns globally in 2016. Another 4OO campaigns were launched by “occasional” activists. Indeed, a fair number of companies should expect a knock at their door soon—21% of the S&P 500 were approached publicly by an activist in 2016 according to Factset (and many others received quiet, private overtures). Such activism will likely grow more prevalent, as it has proven to generate alpha (i.e. uncorrelated returns) for these funds’ investors.

Activists and activism draw sharp emotional responses: some cheer activists as appropriate scolds of lazy and under-performing Boards; others paint activists as locusts focused solely on short-term strategies. Activism is a natural outgrowth of our markets structure and can be a force for good. All capital markets need a mechanism to “police” strategy selection and Board performance in those rare instances when the corporate governance system does not work.

For the most part our system of corporate governance does work and Boards self-correct to put companies on the optimal strategic path. But the Board mechanism is not perfect: Not all boards are as independent as they ought to be and directors also have some interests, such as director fees and job continuity, that differ from shareholders.

For these reasons and others, activists can and do play an important role as last-resort overseers of the shareholders’ interests, but as in every human endeavour, some perform better than others.

Activist techniques were once used only by specialist funds. Now, traditional, long-term investors are adopting (and adapting) activist techniques, increasing the volume of shareholder engagements. They’ve seen that engagement at companies with sub-optimal strategies or under-performing management teams can help generate alpha. It can also help justify the larger fees charged by active managers. At the same time, some specialized activist funds are taking a longer term view of performance.

All of these factors are driving a new wave of shareholder activism, with campaigns often reaching outside traditional targets. Companies of all sizes and types can have “opinionated” stockholders.

Today, in fact, even good stock performance does not immunize a company. Take the recent example of restaurant chain Buffalo Wild Wings. Over the 14 years since the company went public in 2006, the stock compounded shareholders’ money by 24% per year, dramatically outperforming its casual dining peers. On operating metrics, the business also outperformed nearly all of its peers. In the three years before this spring’s proxy battle the stock was up 18% in a difficult sector, in which many of its peers had gone belly up. Yet. Even strong performance like this did not protect Buffalo Wild Wings from Marcato Capital‘s advances and demands.

FUNDAMENTAL DRIVERS

What are the drivers of activist campaigns? Activists are, first and foremost, investors. They seek great returns and they propose changes that they believe will drive better future performance than the market expects. In this way, the driver of activist activity is really the perception that corporate plans are suboptimal plans, not suboptimal past performance. The tactical focus is often on strategy, operations, the balance sheet, business configuration, the board and M&A.

Activists are often extremely knowledgeable about the company, very invested in future outcomes and equipped with analytical tools that can outstrip even a well-meaning board.

Ultimately an activist must be able to answer the question: why hasn’t the board adopted the proposed changes? And so, activists necessarily focus on perceived deficiencies in board composition or on a claim that the board is “stale.” Naturally then, boards with longer average director tenure are significantly more vulnerable to campaigns. If there is a deficiency in strategy or business configuration and the Board is seen as “stale,” the activist can claim the staleness has led to the suboptimal choices.

Activist campaigns are remarkably successful, in part because activists get to pick their targets. In well over half of the campaigns, significant changes are driven by the activist. CEO tenures are shorter and, according to some academics, stock performance is better, once an activist appears.

A 2017 survey by FTI Consulting finds that settlements have become more prevalent and have come quicker than in the past. Nevertheless, more fights in absolute numbers went to a final vote in 2016 than at any time since 2010.

The increased number of companies facing activist campaigns has been driven by non-traditional activists. Mainstream, long-only institutional investors and first-time or “occasional” activists account for nearly all the increased volume in activism. Recent examples include campaigns by Neuberger Berman, T. Rowe Price and PAR Capital Management, all three of which had been regarded as traditional investors that “vote with their feet” rather than vocally.

Activism is becoming a tactic deployed by all types of investors rather than a “strategy” that defines a fund. Along with its broader adoption, the practice of activism has professionalized, with a bevy of advisors that help both investors and companies to engage in these campaigns.

Given the willingness of more investors to use activist tactics, every public company may have “activists” in its shareholder base. The lurking activist may not have a familiar activist fund name: it may be your long tenured shareholder that wants to be heard. Some “activists” are hidden in plain sight.

PLANNING STRATEGICALLY

For public company board members these changes bring a new reality of engaged investors, with heightened reputational stakes for directors. Noisy public campaigns challenge the judgment and composition of the board. And proxy fights are more distracting and expensive than is often imagined. In fact, it’s hard to overstate the all-consuming nature of such battles. Having been involved in more than fifty activist campaigns, we can tell you definitively that once embroiled in a proxy fight, the CEO. CFO, and board members will be forced to spend substantial time dealing with tough daily decisions and the costs often run between $4 million to $6 million for a full campaign at a mid-cap company. These costs have been escalating as campaigns go on longer and often involve many advisors; some protracted fights will cost a company well over $20 million. Obviously, some battles are worth fighting, but remember the odds: Companies very often lose – and will get stuck with the bill and distraction anyway.

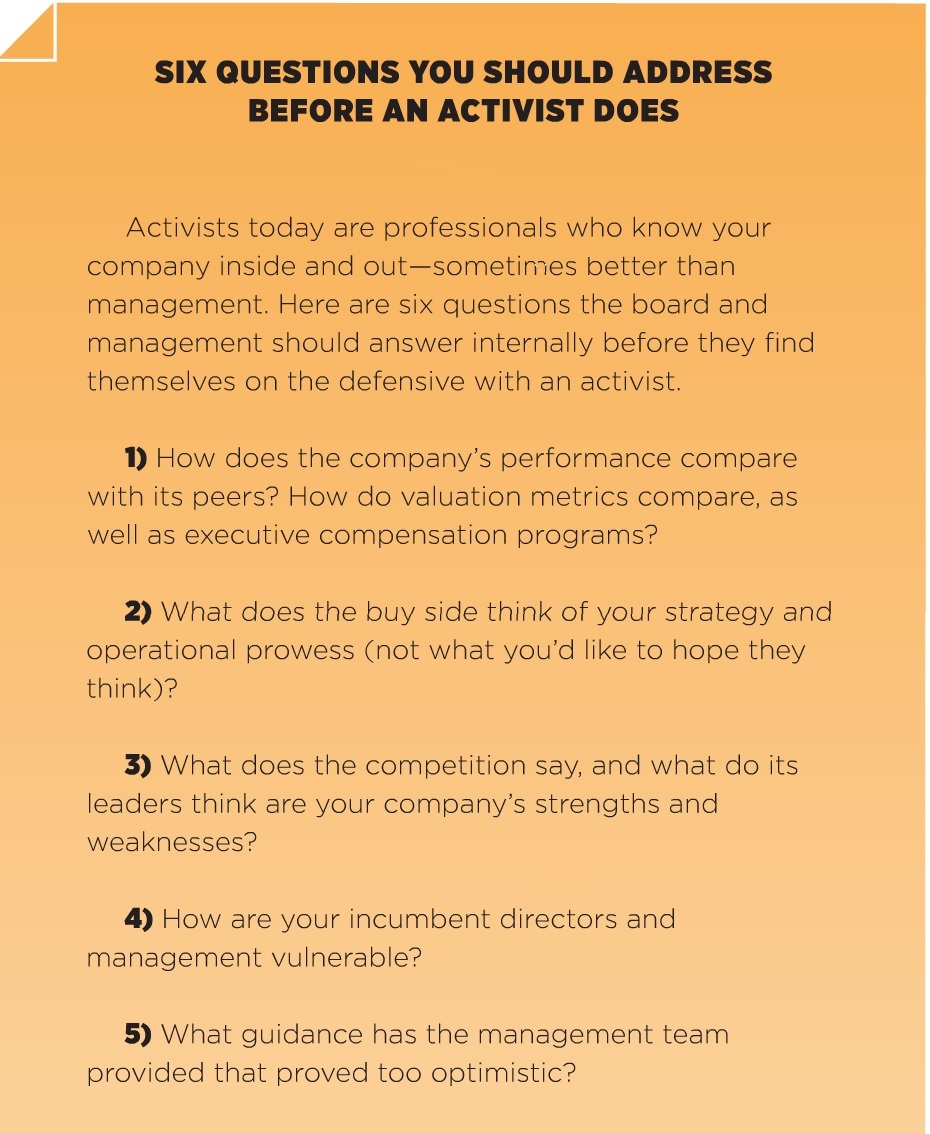

The best defense is to make smart governance moves in times of peace. Since long-tenured boards have proven to be an easy wedge for activists, boards must proactively consider their refreshment, casting a critical eye on the mix of tenures and expertise. Think about setting a target “average tenure” for the board as a governance policy. It’s rare to find a well-composed, self-refreshing board come under successful attack from an activist.

Structural and strategic moves also help avoid activist campaigns before they begin. The board and management should lead an active, objective review and analysis of popular activist hot-button issues (e.g., capital allocation, capital structure, strategy, operational plans, executive compensation, business configuration, personnel, etc.). One good option is to bring in a third party to help the board “think like an activist” to provide fresh input and objective thinking and identify vulnerabilities (which can be opportunities for improvement) ahead of time.

Creative thinking on investor relations is also crucial. Consider “radical transparency” with investors about the roads taken and the roads not taken. Why did your company take a different path than peer companies? Directors must be prepared to provide a rationale about choices made and differences in operating models, strategies, or performance.

RESPONSE TACTICS THAT WORK

RESPONSE TACTICS THAT WORK

Even with the above tactics, a surprise activist campaign involving your company is always possible. How do you respond? As a first step, the board should be immediately informed, ensure there is a response team, and designate a representative to liaison with the team.

Most companies turn to their corporate counsel first. And while counsel is critical in these situations, remember that an opinionated investor is not primarily a legal problem. Advisors can be helpful, but too many can be unwieldy.

It is critical to know where your other shareholders stand on the points raised by the activist. But, be cautious in assuming management knows the true feelings of your shareholder base. Investors don’t always tell their true feelings to management.

The management team should actively engage with would-be activists to understand their thesis and points of view. At first, activists almost always seem friendly and express a desire to engage “constructively.” Be wary. At the same time, always remember that being gracious pays off.

The company must contemplate its approach and words carefully, depending on the activist. Your board can prove a great asset in this engagement. Ensure that one or more directors are designated to speak to investors, should the need arise. (We recognize that many corporate advisers prefer to hide the board from investors. This approach, though common, has serious risks in our experience. Directors are shareholders’ representatives and should be willing to meet with those whom they represent.) Whomever speaks for the company should know that there may be a tricky dance required to be both open and compliant with disclosure rules. This is especially true because activists often suggest things that are actively being considered or are under way, which makes for difficult conversations if the company’s activities are not already public.

In meeting with the activist, avoid defensiveness and a closed mind. Consider elements from an activist’s agenda that you can adopt, leaving him or her with fewer complaints and suggestions. Activist investors often have reasonable ideas worth considering, so be open to contemplating those ideas objectively.

The hardest “suggestions” usually are requests for changes to the board. As noted earlier, pre-emptive board refreshment is often the best medicine. Post-activist unilateral appointment of new directors is certainly not as good as pre-emptive board refreshment, but it’s still better in many cases than remaining static with a board slate that is difficult to defend. Consider the options of agreeing to a third-party board candidate approved by both sides, setting a plan of refreshment, or appointing an alternative stockholder representative.

If you find yourself embroiled in a full, public proxy battle, early moves and press releases will set the tone and shape the future course, so contemplate them carefully with input from advisors. We generally believe that canned press releases or attacks on the activist do not work. Today’s capital markets are sophisticated about activism, and these tactics, along with ad hominem attacks or pro forma pledges of fidelity to shareholders, no longer help a company.

Moreover, tactics from a bygone era are usually received poorly by shareholders and likely will be counterproductive. Suing an investor, for example, is almost always a bad idea. Adopting a poison pill, changing advance notice provisions, or adopting last-minute bylaw changes to thwart a shareholder also generally backfire. Shareholders now expect a substantive response to criticisms and suggestions. Respond to the shareholder on the merits.

Governance responses that work include the following:

- provide transparent, honest disclosures about the board’s rationale for its decisions and actions;

- demonstrate recognition of performance challenges with a clear plan for fixing them; and

- show how value will be created with the current plan, capital structure, management, and incentives.

Careful analysis of your shareholder base can prove critical in knowing how to shape the message and win votes. Stock surveillance services can aid in watching trading to ensure management knows where the stock is.

Finally, be sure to use the independent directors’ voice, especially if there is a strong history of board self-refreshment and shareholder board support. Use a director to sit down with shareholders and explain strategy (and paths not taken), operational performance, executive pay plan design and succession planning. Show the shareholders that the Board is thinking actively about all of these critical areas and working hard on behalf of shareholders.

BE PROACTIVE AND VIGILANT

There’s no doubt the past decade has seen enormous change in the relationship between shareholders, management teams, and boards. In this new era, more than ever, it is important for boards to be well composed, for companies to contemplate all value creation opportunities and for all capital market actors to recognize that good ideas can originate both inside and outside the company.

Smart corporations take the lead, shaking up their own strategies, boards, governance, and engagement rules—before activists force them to.

ABOUT THE AUTHORS

Greg Taxin is the Managing Member of Spotlight Advisors, which advises in activist shareholder situations including in six proxy fights that went to a vote in 2017. He is a former investment banker, lawyer, activist investor and CEO of proxy advisor Glass, Lewis & Co.

Betsy Atkins has served on more than a dozen public company boards, is a three-time CEO, serial entrepreneur, and founder of Baja Ventures. She currently sits on the boards of Cognizant, SL Green, HD Supply, Schneider Electric, and Volvo.

This article was originally published in “Corporate Board Member” 3Q 2017 and has been re-published with permission.

related content:

Activism’s New Rules (Sept 2017)

The Year in Activism Infographic (May 2017)

Quotations of the Day from “Activist Investing in Europe” Conference (Sept 2016)

Best Practice for Activists Dealing with the CEO (Sept 2016)