By Melina Sanchez, Novus Partners, Inc.

Are hedge funds good at timing sectors? Yes. Except when it comes to Financials.

Over the past 10 years hedge funds have beaten the market. Does this mean they’re skilled, or just lucky? We can confidently say there’s one reason for hedge funds to exist: they generate excess returns by actively choosing sectors.

However, this is not the case for every sector. Next, we’ll attempt to answer the following questions:

• Are there opportunities in actively shifting sector exposure?

• How much do hedge funds generate through their sector decisions?

• Are hedge funds better at overweighting/underweighting some sectors rather than others?

Are There Opportunities in Actively Shifting Sector Exposure?

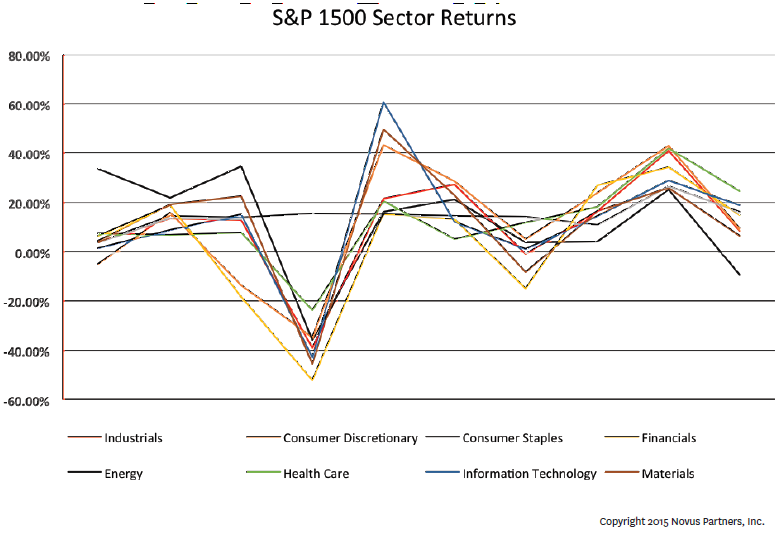

Timing the broad market is difficult, just as it’s difficult to predict specific sector and stock movements. Hedge funds, especially generalists, make sector bets more often than not. Is there enough return dispersion for this strategy to outperform the market? Let’s look at bench¬mark returns for each of the main S&P 1500 sectors:

The average standard deviation for sector returns over the last 10 years is 11.63%.

Thus, we can answer our first question: sector returns are sufficiently dispersed as to enable augmenting returns by actively choosing where to invest.

Do Hedge Funds Take The Opportunities to Actively Shifting Sector Exposure?

So hedge funds could make money by choosing sectors. But do they? And if so, how much?

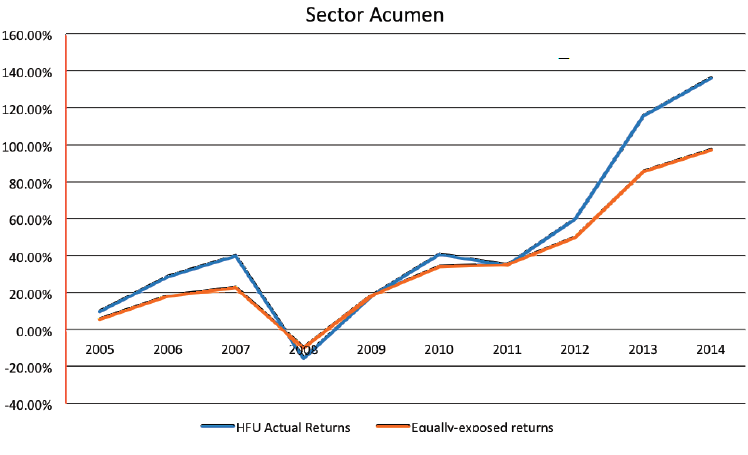

To answer these questions, it’s best to compare the returns of our Hedge Fund Universe (HFU), which includes ~1100 managers, and the hypothetical returns of the HFU had it been equally exposed to the different sectors of the market benchmark (S&P 1500). The answer is in the following cumulative graph:

Compared to an equally-exposed portfolio, where sector exposures are equal to the benchmark’s exposures, the HFU added 3,898 bps of cumulative value over the last decade. Had the HFU invested in the S&P 1500 alone, it wouldn’t have performed as well.

Thus, we can answer our second question: Hedge Funds generate excess returns by actively selecting sector exposure.

Are Hedge Funds Better at Overweighting/Underweighting Some Sectors Than Others?

We now know there are opportunities in selecting sectors and that Hedge Funds have reaped the benefits of these opportunities. The last question is, then, whether hedge funds are good at extracting value from all sectors, or from a select few?

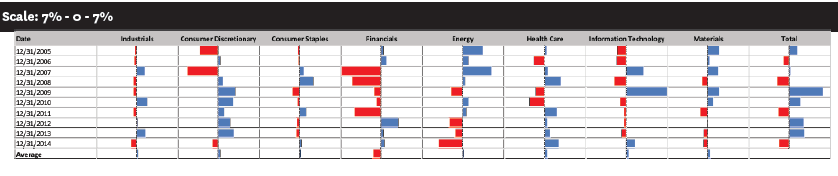

The next chart shows the relative weight of the HFU exposure to the different sectors (= HFU sector exposure – Benchmark sector exposure, in %):

(click on graphic for enlarged image)

(click on graphic for enlarged image)

Over the last decade, hedge funds have predominantly underweighted Consumer Staples and Information Technology, while they consistently overweighted Consumer Discretionary and Materials. Were these decisions additive?

The second chart looks at the value added (excess returns in %) that HFU generated through overweighting/underweighting sectors relative to the benchmark:

(click on graphic for enlarged image)

(click on graphic for enlarged image)

In Conclusion

From this information, we can derive some unique insights:

On average, the shifts in exposures have been positive for all sectors except for Financials. Financials had the largest drawdown, from 2007 to 2011 (around the crisis).

In the case of Energy, Hedge Funds would have been better underweighting it every year. The 2007 bet on Consumer Discretionary hurt hedge funds the most, after Financials.

In 2014, the worst year for hedge funds, managers detracted performance through their sector decisions.

Thus, we can answer our third question: Hedge Funds are good at betting on all sectors, on average, except for Financials.

Copyright 2015 Novus Partners, Inc.. All rights reserved.

About Novus Partners:

The Novus Platform™ is the world’s most advanced portfolio analytics and intelligence platform designed to help institutional investors consistently generate higher returns. The platform is used the top hedge funds, fund of funds, pensions plans, sovereign wealth funds and endowments around the world to analyze risk, performance and attribution and conduct portfolio research across aggregated and historical data sets. Portfolio managers, investor relations teams and operations teams use the Novus Platform in different ways, but ultimately to generate more alpha, analyze and manage their risks, report to their investors and become more efficient with resources. find out more at www.novus.com

related articles: