By Aimee F. Kish and Kurt L. Braitberg of TeamCo Advisers.

_______________________________________________

In 2013, Argentine debt was badly battered. The bonds, which had defaulted and subsequently been renegotiated over a decade earlier, began to crumble. The 7% of debt holders who refused to convert to the new terms became locked in a legal battle with the Argentine government over payment now that the country was recovering. Alternatively, those who had cooperated, the converted bond holders, argued for their right to be prioritized over those who held out. Between Argentina and its bond holders, turmoil reigned.

Despite the apprehension many market participants felt toward the nation’s debt, a U.S.-based hedge fund manager saw the potential for previously untapped profits. However, to realize these profits, the manager would have to act beyond the liquidity and size constraints of its flagship fund, which was not appropriate for an upsized position, due to the opportunity’s complex nature and unpredictable time horizon.

The solution came from outside the traditional hedge fund construct by creating a separate vehicle to match the uncertain liquidity profile of the debt while having the added benefit of also aligning investor interests. The manager invited a select group of existing investors in its flagship fund to join a “special situations fund” (SSF) and paired a relatively illiquid commitment/call down structure with lower fees. Even with the trepidation surrounding Argentina, the manager’s concept drew ten investors who committed capital in pursuit of the deep value investment prospect. Capital was called, invested, and distributed within 18 months with an IRR of 23%.1

This and similar enticing scenarios have helped propel SSFs to the forefront of the alternatives universe across the globe. SSFs provide the means to gain exclusive entrance into funds with idiosyncratic investment mandates engineered by some of the world’s most successful asset managers. Institutional investors are finding these SSFs compelling for many reasons:

• Listed fees are often lower than those in more liquid hedge funds, as well as private equity funds.

• Capital is primarily called and fees assessed only at investment; in some cases, if a manager believes an opportunity set has diminished, capital is never called, no fees are assessed, and the fund is dissolved.

• By focusing on long-term results rather than short-term market movements, SSFs regularly achieve returns uncorrelated to broader markets.

• Target IRRs are up to 25%.

• The manager typically is the largest investor, an indication of confidence in the idea’s merit.

The potential rewards in low return environments are tantalizing for investors considering an allocation to SSFs, but analyzing and evaluating these hybrid funds can be challenged by time constraints and the relative opacity with which SSFs are perceived by many institutions’ constituencies. This paper aims to clarify the structural, operational, and beneficial aspects of special situations funds to allow institutional investors and their stakeholders to more completely evaluate these funds.

OPPORTUNITIES

Special situations funds provide managers with a vehicle able to take advantage of investment opportunities which are generally illiquid and can be inappropriate for liquid hedge funds.

A special situations fund is an investment vehicle created for unique or fleeting opportunities that do not fit within the framework of existing hedge fund structural limits. These parameters may be liquidity constraints, concentration limitations, themes, or a combination. Rather than an untested idea, an SSF is typically related to an existing strategy or position already expressed in a flagship fund.

Hedge fund general partners (GPs) often constitute up to 25% of SSF commitments themselves, strongly aligning manager interests with those of investors. Significant GP participation increases the likelihood that managers will launch funds only when special opportunities exist and will exit when target investments are ideally mature or fail to materialize. SSFs most often stem from a concept a GP has explored, is comfortable with, and sees the potential for returns in the near future.

Special situations funds fall under the broad category of “co-investments.” In co-investment funds, a small number of investors join a manager in an exclusive and specific opportunity. Co-invests may sound familiar to private equity investors; however, while private equity co-investments generally focus on a single, one-off deal such as a real estate or a business purchase, hedge fund SSFs often follow broader themes or investment strategies that include a diversified group of investments.

An example of a broad theme an SSF may target would be the de-risking of the banking sector. Financial distress can play a key role by way of forced sellers, including banks, insurance companies, and asset managers, as well as borrowers for whom a bank loan is not appropriate. Numerous SSFs have focused on credit oriented strategies, representing a source of capital or one of a few knowledgeable buyers of complicated structures. Related credit focused themes pursued by SSFs can include direct lending, leveraged loans, distressed securities, structured credit, asset-backed securities, and residential and commercial mortgage securities.

CASE STUDY: BULL IN A BEAR MARKET

During the financial crisis, mortgage-backed securities and similar structured products became largely unpopular. Investors fled from such exposures and the resulting markdowns of value sent reverberations throughout the entire alternatives market. The industry looked on MBS with a bearish eye. An opportunistic manager considered this and predicted the trend to be of a moderate duration with a subsequent reversal. In the fourth quarter of 2008, the manager launched a concentrated market dislocation strategy to participate in MBS and similar debt instruments. Offering the fund at a 1% management fee and a five year commitment period, the final assets were sold in 2013 to realize a net IRR of over 20%.2

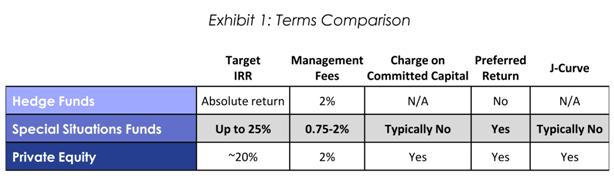

TERMS

Special situations funds typically charge solely on called capital, avoid J-Curves, charge management fees from 0.75%-2%, target IRRs up to 25%, and offer preferred returns.

SSFs are compelling not only for the opportunities they access but also their pricing structure, as Exhibit 1 summarizes. Management fees typically range from 0.75% to 2%, and are generally less than those of the firm’s flagship fund. Moreover, fees are often charged only on called capital, unlike private equity.

Since special situations funds play off the strengths and expertise of fund managers by pursuing investments or themes typically already expressed in the flagship fund, the costs necessary to explore these investments are much lower. This allows the manager to often charge only a management fee once capital is called and put to work. At the time of fund launch, much of the preparation for the SSF investment has already been completed. This arrangement helps avoid the dreaded J-curve return profile (drawdowns at the start and returns appearing in later years). So while both private equity funds and SSFs take commitments up front, private equity managers collect fees throughout the time they are identifying investment opportunities, whereas a SSF is typically launched once a specific investment opportunity is identified. In certain isolated cases where a concept never fully materializes, a manager may wind down the SSF without ever calling capital or charging fees – a unique, aligned, and investor-friendly attribute.

Hedge fund investors will also find the SSF performance fee, or carried interest, structure appealing. SSF performance fees are generally between 15% and 20% and are charged on profits in excess of specified hurdle rates. This is in contrast to hedge fund flagship returns which do not have a target rate of return. In many SSFs, target rates are between 7-8%. In all, the assessed fees can be expected to be lower than those in either a private equity fund or a more liquid hedge fund run by the same manager.

CASE STUDY: THE SPANISH ACQUISITION

Often mentioned in the same sentence as Greece, Spain’s future has for many years been dismal in the minds of investors. While the consequences are numerous, one observable effect was the diminished availability of financing, particularly for real estate investments. While many investors were avoiding Spain, a U.S. manager saw an opportunity to capitalize on the situation and secure a sizable profit in exchange for acting as a source of capital. Partnering with a Spanish private equity firm focused on real estate,the investor developed a European direct lending SSF. With a total commitment of roughly $200M, the fund launched in August of 2014. By early 2015, the fund had accumulated a net IRR of approximately 10%.3

CLASSIFICATION

Special situations funds can be difficult to categorize in a portfolio under private equity or hedge fund classifications, but their diverse traits can stabilize and improve an overall investment program.

The diverse traits of SSFs may provide a balancing element to an overall investment program, but this same diversity can also create problems when placing the investment into an asset taxonomy which is typically delineated by degrees of liquidity (i.e. liquid versus nonliquid). SSFs general investment periods, fee schedules, target returns, and liquidity blend two poles of the alternatives world.

It is difficult to specifically define an SSF due to their idiosyncratic nature and the fact that they straddle two different investment landscapes. Many institutional investors struggle with the appropriate classification for such funds as the time horizon of SSFs falls somewhere between that of liquid markets (1-12 months) and private equity funds (8-12 years), as illustrated in Exhibit 2. SSF terms typically run 4-6 years. Investment holding periods tend to span between six months and four years, with exits realized through a variety of strategies such as liquidation, contract maturity, refinancing, or IPO. The blurred lines between hedge fund and private equity and liquid and illiquid often forces investors to attempt to fit a square peg in a round hole.

*This provides a list of the potential investment types that may be represented in a special situations fund. No assurance can be given that any potential investor will have a special situations portfolio constructed from any of the investment focuses listed above.

The longer investment horizons of SSFs give them hybrid characteristics of both private equity and hedge funds. The manager is afforded the latitude to invest in less liquid markets and wait for an optimal time to exit. Generally, this leads to returns uncorrelated with other hedge fund returns or other liquid investments.

But, the longer time horizon and resultant reduced liquidity prompt some institutional investors to place SSFs within a private equity apportionment, thereby classifying what may be 4-6 year private debt within an 8-12 year private equity segment. While this captures the relative illiquidity of the investment as compared with hedge funds, it can also be problematic. The parameters of private equity and hedge fund investment styles usually differ fundamentally. Private equity vehicles commonly seek a higher return but with higher liquidity constraints, different investment strategies, vintage year considerations, and potentially different capital call cadence and other nuances. Grouping SSFs as part of a larger private equity allocation strategy could possibly over (or under) emphasize some investment characteristics in portfolio management, analysis, and planning.

Contrarily, neither are SSFs completely hedge funds. With lengthier lockups and the prevalence of more private market deals, special situations funds can be uncorrelated with public market returns. While this is true of many hedge funds, SSFs may exhibit exacerbated nonconformity to many benchmarking strategies. This is often one of the compelling aspects of these funds; however, considering SSFs as hedge funds in portfolio management and planning might prove misleading when trying to understand portfolio exposures and behaviors.

While there is no clear-cut classification that can be prescribed for SSFs, institutional investors must weigh the pitfalls of the difference between a hedge fund and private equity categorization in light of their overall portfolio. Alternatively, SSFs can be pocketed in their own bucket outside of both realms. Regardless, the potential benefits of SSFs in an investment program should encourage investors to incorporate these funds into their portfolios.

PREVALENCE

Special situations funds’ popularity is growing, as managers source increasingly beneficial ideas; as the prevalence of these funds rises, allocators must carefully choose the best SSF for their portfolio.

Due to their uncorrelated nature, liquidity structure, fee structure, and targeted returns, institutional investors are creating a growing demand for SSFs and fund managers are responding with supply. In a 2014 survey, J.P. Morgan found that nearly 74% of endowments and foundations, 68% of consultants, and 60% of pensions would participate in a co-investment situation.4 When Aksia queried 198 hedge funds representing $1 trillion in assets under management in 2013, 50% of the firms said they were either managing co-investments or would consider offering them.5

This rise in supply and demand has forced SSFs from a narrow niche in which managers extended invitations to select institutional investors to a wider and more diverse investor base. Some SSFs coming to market are lacking the sharp focus and specific investment theses of their more exclusive counterparts. The lack of usual barriers to entry for many managers may be an indication that SSFs are being manufactured more as asset receptacles for a broader firm strategy than as immediate, narrow investment opportunities for GPs and select LPs. As a result of this increased availability, investors weighing SSFs need to be particularly attentive to the style, structure, and intent of managers launching and marketing funds.

Yet, the exclusivity and sporadic nature of SSFs make them difficult to analyze. Without published indices, publicly available data is unaccommodating. In addition, managers habitually do not distribute historical returns for their special situations funds as they are, by their very nature, private closed funds. Further, pre 2008 SSF-like returns are often historically embedded in the return stream of flagship funds.

Due diligence demands are also exacerbated as SSFs frequently require a rapid launch to exploit fleeting windows of opportunity. Institutional investors need to remain on guard and carefully evaluate the manager prior to analyzing any special situations fund, no matter how tempting the investment prospect. For institutional investors, the return profile and degree of (un)correlation with liquid markets will change with each SSF explored. The consideration of the investment thesis is, of course, paramount as is an understanding of the investment manager’s track record of investing in less liquid markets, and their back office control and infrastructure.

CONCLUSION

Special situations funds are a flexible and dynamic means for hedge fund managers to make less liquid but potentially higher performing investments. SSFs tendency to invest in less liquid opportunities can provide returns uncorrelated to liquid markets, potentially diversifying, balancing, or fortifying a portfolio. The space between the liquid and the illiquid is vast and rich with opportunities. As seen in the profiled case studies, managers have been taking advantage of these opportunities in a variety of ways, ranging from structured credit to direct lending. With an aligned structure, reduced fees, and stable investor base, institutional investors can be dazzled by the SSF prospects of these attributes in conjunction with the compelling returns.

Nevertheless, investors need to carefully consider the exchange of liquidity for the potential of enhanced returns within the context of their own portfolios. Only after institutional investors have conviction in a fund manager, should the investment thesis of an SSF be considered. SSFs offer the means to take advantage of an enticing investment opportunity and require the skill and expertise of a manager with high integrity, leadership skills, and intellect for the potential of success.

This analysis and review are being provided for informational purposes only and should not be considered either an offer of or a solicitation to purchase or participate in any of the particular services or securities referred to herein. This article and the paper on which it is based are not offers to sell or a solicitation of offers to buy any security, including interests in any private fund TeamCo may now or in the future offer.

1, 2 and 3 This example is based on an actual SSF. This is not an investment in which TeamCo, or its clients, participated. The manager names have been omitted to avoid potential conflicts or other issues.

4 J.P. Morgan, “Aligning Interests: The Emergence of Hedge Fund Co-Investment Vehicles,” First Quarter 2014.

5 Aksia, “2014 Hedge Fund Survey,” conducted during the end of October and early November 2013.

Related articles: