By Simon Kerr, Publisher of Hedge Fund Insight

Neil Meadows categorises global macro managers into two types – tactical managers and thematic managers. Classic tactical managers would be the Palindrome (George Soros), Mike Novogratz of Fortress and George Papamarkakis of North Asset Management. Examples of thematic managers given by Meadows are Guillaume Fonkenell of Pharo Management and Peter Thiel of Clarium. Neil Meadows himself is in the thematic peer group of macro managers with his Laurentia Global Fund.

Neil Meadows – Illustration by Hedge Fund Insight

It is rare for a hedge fund manager to know their competition quite so well as to be able to divide them into sub-categories, and, further, to be capable of detailing their respective added value as investors and how they operate their approaches to risk management, but then Neil Meadows has a very rare perspective on what he does from his previous work experience. He is a critic who has become a playwright. Or, extending the metaphor, he is a former screenwriter and drama critic who is now writing plays.

Meadows has long experience of markets and investing having first worked on the sell-side in fixed income derivatives for Merrill Lynch in New York back in 1994. He was then a successful fixed income prop trader for DKB Mizuho in London for 8 years (the screen writer analogy), and then went on to invest in hedge funds for funds of hedge funds for 6 years (the drama critic part). In the latter role Meadows had the opportunity to see first-hand how top-tier macro managers operate – how they organise their portfolios, control outcomes, and source ideas. This is a credible c.v. for a macro manager, but it is not archetypal.

What is typical is that the Laurentia Global Fund has the mandate to invest across the asset classes (FX, bonds, equities and commodities) and invests at the market level using very liquid instruments. There is no credit risk taken as the fixed income exposures are in G7 government bonds, and when equity exposure is taken it is in the form of index futures rather than attempting to select individual equities.

The Laurentia fund has a target return of 12-15% annually, with “a risk allowance or drawdown” based on a 3-to-1 ratio of 5% for a single month. This is a scaled-back risk assumption versus the first generation of macro managers, who would look to make 25%-plus returns for which a 10% loss was perceived as tolerable. The old style macro managers could have, say, 8x leverage, whilst the modern form of macro management practised by Laurentia Management employs limited leverage. “For a zero interest rate environment, and a lot of weight put by investors on the smoothness of returns, a return of 12-15% is attractive,” says Meadows. “That rate of return will double investors money in less than 7 years.”

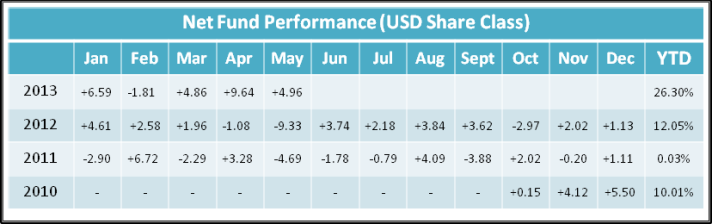

To date the target returns have been surpassed, and Neil Meadows says that there will be periods in the future when the run rate is over 15% and periods when returns are a lot less. Indeed the pattern of return has been better than some old style macro managers, as the Laurentia Global Fund has had 67% positive months in its 32 months of trading. The returns since inception in October 2010 are given in the table below.

Table 1.

Source: Laurentia Management Limited

The skew in the return profile is due to risk management on the downside, and, on the upside, a willingness to use some leverage and stick to positions “when the policy environment is clearer,” according to Meadows. The two drivers of skew will be examined further.

Risk Management

Starting with the risk management employed; Laurentia applies a risk envelope which includes VaR targets and an upper limit to VaR. The target VaR is 2.5% (all VaR estimates are based on 1-day horizon with a 95% confidence interval). The maximum daily VaR is 4.5%, based on a 2 year look-back window. Concentration limits per asset class, are expressed by the manager as a percentage of risk. The fixed income investments of the Laurentia fund can be up to 100% of risk taken. Currency positions can be up to 75% of risk, equity indices can be 85% of risk, and commodities may be up to 70% of risk taken. This set of boundaries of concentration risk by asset class is set to bring about a small amount of diversification by asset class, but does not force meaningful diversification. Rather, it relates to volatility of the asset classes.

Laurentia uses two levels of indicative stops. At the position level the maximum indicative loss to the NAV is 3.5%. At the fund level the indicative stop loss is 7.5% for the month..

The bias to positive returns in the 32 month history of the Laurentia Global Fund is brought about by a number of things – the hit rate of the manager, the holding period, the feedback loops, the directionality, and the willingness to add to positions, reduce risk, and take profit.

Each month the Fund has traded there has been a point in the month when the NAV was up by 1% or more. The outcomes for the end of month NAV are, on the downside, a function of the risk management disciplines to curtail losses in volatile markets, and on the upside a function of the portfolio manager’s feedback loop and conviction as expressed in position size.

Fundamentals, Fundamentals, Fundamentals

Periodically investment managers get forced to review their investment hypothesis by the short term P&L. Even if a position has made a lot of money for the fund, if the recent period P&L is negative then the base case for having the position has to be revisited. In the instance of the Laurentia fund Neil Meadows owns positions for fundamental reasons and will check if a new analysis of the fundamentals shows the same policy implications as were the case when the position was initiated. By contrast a tactically-centred macro trader will check if the market positioning and flow information of his position are still as they should be (positive for a long and negative for a short). It is a key differentiator that the feedback loop for the Laurentia Global Opportunity Fund is a fundamental one.

Neil Meadows – Illustration by Hedge Fund Insight

Meadows shows his strong bias to fundamental analysis in that if his analysis has been vindicated since the position was initiated then he may add to the position (even if it has a negative short term P&L). For example, after reading two speeches in a week from members of the Bank of Japan that were consistent with the view already expressed in his portfolio Neil Meadows added to his Japan-related positions, as his conviction had increased. This is less likely to be done for an FX trade, where Meadows likes to see market price action support his trades before he adds.

In terms of sizing a currency position, it may be initiated at say a 35% of NAV. In the course of three additions that could be at 85% of NAV at book cost. Such a position would be put on over a 3 to 4 month period with the intention of holding the position for 9 to 15 months. A currency trade would be put on looking for specific events to happen subsequently. These events are then catalysts for further addition (or reduction) to the position.

Another facet of the approach that potentiates the upside is that the portfolio manager of the Laurentia fund only trades outright directional positions. Many macro managers like to run investment strategies of different risk/return profiles – positive carry strategies and/or spread trades, plus core directional strategies. The thinking of the other macro managers is that the three types of strategies run in tandem give the potential for a smoother return track record. Meadows’ fund only takes directional trades in part because the simplicity of the strategy is easier to manage, but is more that the directional methods of implementing views are a better fit with how the manager thinks about investment opportunities with the right risk to reward.

There is a very large focus on fundamentals in the investment process of Laurentia Management Limited, and the activities of central bank and political decision-makers are the main study area of Neil Meadows’ analysis. This specialisation is unusual for a macro manager. The proportionate allocation of research time of Meadows is given in the graphic 1 below.

Graphic 1. How Research Time Is Used

Source: Hedge Fund Insight/Laurentia Management Limited

More than half of research time is devoted to tracking and analysing central bank policy. Meadows tracks the activity and public pronouncements of the key decision makers at the ECB, The Federal Reserve, the Bank of England, The Bank of Japan, (Bank of China?), and Bundesbank. The rest of the research time is allocated equally to macroeconomic research and the political process. Neil Meadows generates a road map of where the large economic blocs are headed from understanding from where they have come, and in which way the levers of power are forcing change. Monetary policy is the main tool of central banks, but it impacts real economies with a lag. So a current take on central bank policy and policy change will be reflected in outcomes over the next year to 18 months. This is the forecasting window of Laurentia.

The activities of government decision makers and politicians are tracked by Neil Meadows to see where public policy is going to impinge on central bank activity, and bring about change at the macroeconomic level. It is the combination of the three elements of research that is the USP of Laurentia Management Limited.

Turning to the investment decision making at the firm, Meadows puts a similar emphasis on the fundamental inputs of putting on and taking off a position as he does to the allocation of research time. There is a clear bias towards the real world activities and pronouncements and macro policy changes in the ranking of inputs to the decision-making process given in the table 2 below.

Table 2.

Source: Hedge Fund Insight/ Laurentia Management Limited

It should be emphasised that “geopolitical events” can be things such as the Fukushima nuclear power plant disaster, or the launch of test missiles in various world hotspots. Such geopolitical events tend to be triggers to taking off risk positions promptly to enable a considered assessment of the situation and potential impacts to be made. The events themselves have often presented opportunities to Laurentia as the markets can over-react to newsflow. Indeed Neil Meadows has made money in response to crises like that in October 1998 (LTCM/Russian GKOs).

The majority of global macro managers would put economic indicators and market indicators far higher up the ranking of inputs to their decision making. The preference of other macro managers to do this makes their risk appetite more sensitive to the traded markets, and in particular has resulted in them suffering when markets alternate between phases of risk on and risk off. Neil Meadows reads the fundamentals and then identifies which asset class most simply and most directly reflects the policies identified in the overlap area of graphic 1. Meadows often sees an asset class or a region as offering the best risk/rewards for a period. Having seen Europe as ripe in the first quarter of 2012, the Fund was invested in European equity markets, but since the first quarter of 2013 he expects to be taking more risk in currencies generally, and has been looking more to the Far East, and Japan specifically.

Having decided to commit to a region and/or asset class Meadows will also monitor which market is moving. This is a small element of looking for Sorosian reflexivity in the markets, that is, the market that is moving early or most will continue to do so as other investors spot this.

Assuming Risk Opportunistically

Meadows has enough experience of the hedge fund industry to know that he would not be able to market his hedge fund until it had a two year track record. By the time of writing the Fund has been running for 33 months, and the quality of returns is top tier within the strategy. However, external investors will hesitate because the Fund is very small at $10m, and Neil Meadows is the only investment professional at Laurentia Management Limited. Further Laurentia Management Limited is regulated by the Isle of Man financial authorities, and the fund advisor operates from London.

The style with which the Laurentia Global Fund is run assumes risk. On the day of the first meeting with the fund manager the VaR was 3.3%, and there is a target VaR of 2.5%. With a good hit rate that is enough gross risk to achieve annualised returns of 25% net. However, the manager is willing to go to cash and has done in the life of the fund. The strategy is labelled opportunistic, and has been that in practice – in 2010 profits came from precious metals and commodities, in 2011 (as the US was perceived to be stabilising) Meadows was invested in US large cap equity indexes, and last year the Fund was in Euro STOXX 50 futures . This year most of the risk has been in currencies, including exposure in Japan and within that mostly through pairs with the long on the Dollar side.

The manager says the investment strategy he employs is one that in which there can be infrequent position taking. “I am comfortable to be a trader watching the game,” Meadows explains, “waiting for a catalyst of specific central bank policy announcements as a call for action.” Putting these together, Neil Meadows only invests with conviction. There are no farm team positions (builds) in the Fund.

Neil Meadows’ Laurentia Global Fund has out-performed the declared targets for absolute returns and volatility of those returns. With a significant prevalence of positive months, the longest drawdown limited to three months, and the large monthly returns being mostly positive the track record is marketable and, at this point long enough, to attract capital from any source. This is particularly true when taking account of the investment strategy label, as few global macro funds have produced double digit annual returns over the period in which the Laurentia Fund has invested.

In recent years investors in hedge funds have shown a bias towards macro funds that are very systematic in their appraisal of investment opportunities. These funds have tended to be reasonably well diversified and very large indeed. Laurentia Global Fund is none of these things. It is small, and it is managed by a very small firm that hates the use of models. And it has beaten the returns of most global macro funds in the process.

Neil Meadows has shown an ability to take large bets with conviction and willingness to stick to positions. He says that he has to dance with the markets when necessary, and he has been adept at it. In the next phase of development of Laurentia Funds he needs to take a few steps with a range of potential investors to make the firm as commercially successful in future as it has been at investment in the recent past.

Neil has proven to be a committed, profitable and skillful macro trader.

Neil reminded me of myself when I started Japan Macro Fund in 2000 with a small AUM, and of less than US$10mln for about 4 years. Nevertheless my Fund grew dramatically through consistent strong returns, and AUM peaked at US$850mln in Sept 2009, when I closed the Fund, returning investors with more than net 400% return after 9.5 years.

Neil then FOF firm was one of my investors.

I wish Neil & Laurentia every success.

Your friend,

Chua Soon Hock

Asia Genesis