For just about all of the last decade it has been consistently suggested that the fund of hedge funds sector was just about to consolidate.

Industry watchers suggested that the three different size categories had very different profiles – as potential acquirers and takeover targets. The medium-sized players were going to snap-up their smaller brethren. The larger players were going to add to their assets under management by picking up medium-sized funds, and small funds of funds looked out-moded and should merge or fade away, so it was said and written.

The rationale for consolidation had several arguments:-

1. The industry was mature, as shown by the declining average fees charged.

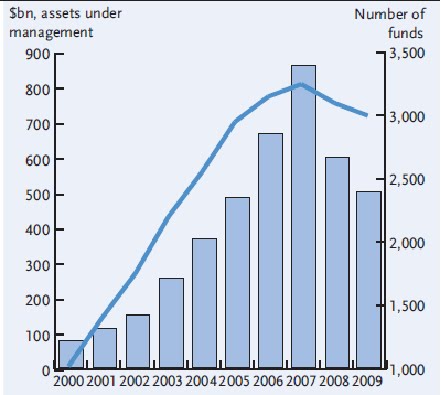

2. Assets under management in funds of hedge funds as a percentage of the whole hedge fund industry peaked as long ago as the middle of 2008.

Graphic 1. Global Fund of Funds Industry

Source:IFSL estimates

3. In 2009 the attrition rate amongst funds of funds was twice the rate of single manager funds at times.

4. The costs of being in the business were on the rise as staff remuneration and the costs of compliance were only going up.

5. Institutional investors were increasingly dominating flows into the industry, and only large scale fund of funds organisations looked of institutional quality.

6. Brand names and critical mass were important to institutional investors and furthermore this client base required high-end (and therefore expensive) risk management systems and risk management professionals.

7. Assets are still leaving funds of hedge funds – according to TrimTabs they lost $17.4 billion in the three months to February 2010.

Several hedge fund firms ran in-house funds of funds that they hoped to commercialise, following the template of Renaissance Technologies’ Meritage Fund, the West Coast fund of funds that was founded to invest partners’ capital in single manager hedge funds. But these “natural extensions” of the business can find it as hard as unconnected funds of funds to get traction. For example, London based money manager Millennium Global closed down its small fund of funds run by Hamlin Lovell in the middle of last year, and Brevan Howard had a good-hard-look at entering the fund of funds business before deciding against it in 2009.

Second, and maybe the larger surprise of the two deals announced for funds of funds last month, was the purchase of a 75.1% stake in Aida Capital by Standard Life Investments. Aida Capital is a London based, FSA registered, fund of hedge funds manager. Aida currently manages the Aida Open-Ended Fund, a Guernsey listed investment vehicle and the Aida Closed-Ended Fund, an investment fund listed on the London Stock Exchange. In total AUM at Aida are around $50m, whilst Standard Life manages around $207bn. A “modest upfront fee” will be paid for the stake. At that scale it is all upside for Standard Life – it will have access to a wider range of alternative investments than before, and new fund of hedge fund products will be created specifically for Standard Life, which may be distributed through recognised life company channels. It is also open for the life company assets to be invested in funds of hedge funds, particularly when the issues of legal structure are resolved in the UCITS III format.

One Response to “Fund of Hedge Funds Consolidation: The gun has been fired”

Read below or add a comment...