By Simon Kerr, Publisher of Hedge Fund Insight

One of the biggest decisions that hedge fund managers in any investment style have to make is how they respond to significant losses, even if they are relative in nature. So think back to the response last year of Paul Tudor Jones in reconfiguring the capital allocations within his funds. Even though he made good money in 2009, his flagship BVI Global Fund was up 16.51% last year, he rejigged allocations – reducing some systematic strategies, cutting out some emerging market exposure altogether and increasing the classic opportunistic trading element. This was intended to be something of return to its roots for the Global Fund, as Tudor Jones himself managed a bigger proportion of the assets, and macro in total was re-emphasised as it made up 88% of Fund assets from the 3Q of last year. The call was that the markets environment would be more suitable to that big-picture type trading that served Tudor Investment Corporation so well in the 90’s, as QE created a time-warp.

This re-think of capital allocations to strategy enabled Tudor to be more nimble in moving capital around in the year since, and since part of the rationale was to enable capital preservation, in that he has broadly succeeded. Tudor’s flagship BVI Fund is up about 3% year to date.

Like systematic CTAs, global macro hedge funds like to ride emergent trends. Macro funds give themselves some scope to argue with markets to a degree, so they will try to buy/sell around turning points of assets based on a macro-economic viewpoint, but the big money money is made from being on trends that persist more so than catching a bottom or top.

Given the switch-back nature of some markets there has been scope to win and lose out of equity exposure. Hard commodities have had both bull and bear phases this year, and softs have become the new game in town for those that didn’t know what a bushel or crop report was a year ago. Put these market outcomes together and no wonder that we have a good range of returns within the universe of macro managers. The meaningless average return was over -5% at the end of July for global macro funds.

As ever there is a path dependency in macro returns – how did the managers respond to their changes in P&L; when did they lock in the gains; and to what degree did they argue with markets? – the responses determined outcomes over the year. One bulge bracket firm that had this challenge this year was Louis Bacon’s Moore Capital Management.

Moore Global Investments, the flagship fund is now up 2.75 per cent for the year as of October 14. The average hedge fund was up 4.8 per cent for the year as of the end of September, according to Hedge Fund Research. Although the gain at Moore Global Investments is modest relative to the hedge fund industry average, it reflects a significant bounceback for the fund from its nadir in May, after the fund was hit by a 9.15 per cent loss in a single month – the worst ever month for the fund.

After such a significant loss even as experienced a hand as Louis Bacon, with a 20-year track record with his own firm, will have had to take a hard look at where their tactics went wrong. The scale of the loss was such that risk management disciplines would have been reviewed for appropriateness, and the allocations of capital within the firm and across the markets assessed in the light of the depletion of investors capital.

Having checked through all these inputs, Louis Bacon took the toughest of the range of responses available. The natural thing to do, indeeed the classic response to preserve capital, is to cut the extent of risk taking. Not just trimming the curve risk of the portfolios – the positions which are outliers in risk terms – but hacking into the core of the portfolio to take Value-at-Risk down by, say, a half. The traditional concept of trading is to take down risk whilst re-assessing the fit of the inherent view of the porfolio with the market environment. This allows more dispassionate views to be taken of the state of play, and the traders can then put risk back on with a refreshed palate for risk assumption.

This is not what Moore Capital did. Instead the positions were maintained, risk levels were unaltered and in effect, a confidence was expressed in the original conception of how they were going to make money for the regime prevailing in markets. After the worst single monthly loss experienced in 20 years it was a very tough call to make, because a continuation of the markets moving against the positions taken would be debilitating psychologically for the traders, and investors would be calling in by ‘phone for comfort to a much greater degree than in the previous month.

Of course it helps that Moore Capital has a 20-year record of delivering big returns to clients. On average, the fund has returned more than 19 per cent annually. But even such a stellar long-term return profile can be challenged by a YTD figure running at minus 7 per cent when other funds have positive returns. It is to Louis Bacon’s credit that he stayed firm enough of his convictions to hold on to positions and bounce back to the extent he has. Tough call, successful call.

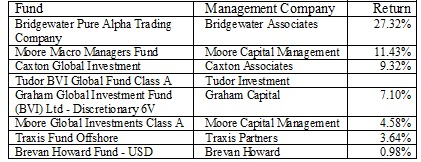

Addition of 28th January 2011: Peer Group Fund Returns for 2010

One Response to “All Credit to Moore Capital for This Year’s Bounce Back”

Read below or add a comment...