By Jerry Haworth, CIO and co-Founder of 36 South Capital Advisors LLP

[In this article the terms “volatility” and “options” are used interchangeably for the purpose of simplicity. Options are really a member of a family of volatility assets]

![]() Everybody loves options, the generic kind. We love to be able to look back and un-decide a course of action without cost, i.e. to return assets after sale and get one’s money back. This is rare in practice though as there always seems to be a cost, seen or unseen, of having optionality in one’s back pocket.

Everybody loves options, the generic kind. We love to be able to look back and un-decide a course of action without cost, i.e. to return assets after sale and get one’s money back. This is rare in practice though as there always seems to be a cost, seen or unseen, of having optionality in one’s back pocket.

Wealth creation is no different: all of us would like to see the outsized returns which great risk brings but don’t want to “suffer the slings and arrows of outrageous fortune” [i] if their investment goes south. However some people do manage to have their cake and eat it too – they source or create this optionality which gives huge upside for little or no downside.

It is this writer’s opinion however that the ability to create optionality is the single biggest wealth driver in the world. For example, thousands of top executives made their money predominantly via share options.

Unfortunately most of us don’t get given options but have to buy them. What is the correct price and when do they represent value?

The options market is huge, about the same size as the global bond market, $66 trillion according to The Bank of International Settlements. Surely there are millions of very clever people ensuring the price is always right? While the price is always right the value rarely is. Paulson, the legendary hedge fund manager, made billions in 2008 betting against subprime using optionality where he could make vast sums investing only a fraction of what he stood to gain. Where were the rocket scientists then? They didn’t see the value, only the price and the price “seemed” right, to the models anyway. The reality on the ground is that globally, opportunities exist in the vast options universe where the price and the value are vastly different. So tactically, there are always opportunities in this space.

Why now?

Greater opportunities exist however due to cyclicality of volatility; in fact it is the major determinant of option’s richness or cheapness. There is “a tide in the affairs of men” [ii] and this is readily apparent in how we cycle between extremes of greed and fear, which directly affect how we price options i.e. the speed at which we cycle between greed and fear results in uncertainty or volatility, which is the major determinant of an option’s price.

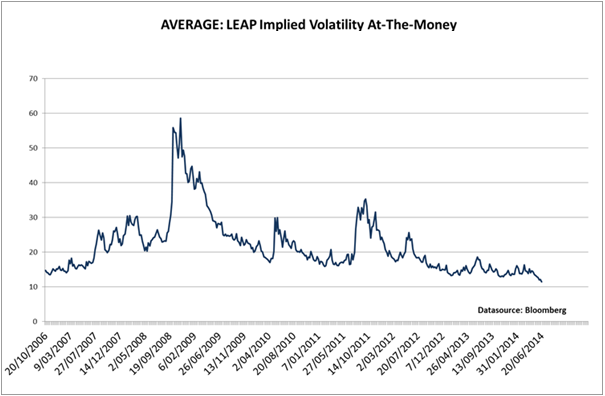

(average of S&P500, NASDAQ 100, Dow Jones Eurostoxx 50, DAX, AEX, SMI, Hang Seng Index, KOSPI 200,

and ASX 200)

The time options that are at their cheapest and their value at their most profound is generally after a long period of calm where option sellers have become complacent and greedy, willing to sell options at well below their “normal” value . This usually occurs just before the end of the era of low volatility as the market cycles to the next regime i.e. high volatility.

Volatility and therefore option prices are at extreme lows not seen since before 2008 across all asset classes. So that answers the “why now?” question. We are at the right stage of the cycle.

Risk/return

Structurally, or due to long term structural factors, option prices can get out-of-whack as well. The elephant in the room these days is low interest rates. The existence of low or zero interest rates has pushed investors to look in far-flung-fields in search of yield: investment professionals, eager to please yield-hungry investors, take risks the average investor does not perceive and package them into products with low but acceptable return BUT mis-priced risk. Savvy investors on the other hand, buy the other side, minimal risk with massive potential return. They understand there is no logical reason to price uncertainty cheaply just because interest rates are low, probably the opposite! Option prices are now unnaturally low with regards to their potential pay-off.

That sums up the “risk/return” reasons to invest in volatility (options) but there is an even more pervasive reason to invest in volatility. Hard to believe but it is true!

Correlation

Correlation benefits which can accrue to almost any traditional portfolio by investing in volatility are rare, unique and valuable. 2008 showed that in a systemic crisis, most assets correlate to one, i.e. all assets losing money together even if they were relatively uncorrelated before. This creates a massive dilemma, diversification is supposed to be the saviour of portfolios in these situations but, in fact, losses are exacerbated as the diversification no longer exists.

Volatility assets however, have a very unique correlation footprint. They tend to correlate to -1 as volatility is inversely correlated with market prices. So as the market falls, volatility generally rises and nearly all long-volatility assets benefit with increasing volatility. Thus they tend to act as a true diversifier in times of severe market stress.

Last but not least is the option’s ability to “snowball” returns, i.e. make returns in increasing amounts the more volatility or directionality increases. This allows them to take the “insurance” role in a portfolio as well. Tail-risk hedging needs financial instruments which can “snowball” or display convexity. It would be pointless to spend $1000 a year on house insurance only to be paid out $1000 in the event of a fire; you need an investment of $1000 that will pay $1,000,000 if the house burns to the ground!

Conclusion

In summary, performance in most portfolios is dependent primarily on risk, return and correlation. Volatility assets can exhibit an exciting risk/return profile with unique correlation tendencies which can make money alongside traditional assets but display their best qualities under stress and extreme market events. They deserve their place in even a traditional portfolio.

Their performance is predicated upon finding great tactical allocations, buying at the right time in a volatility cycle and taking advantage of structural inefficiencies. We believe all three exist “in spades” in the current market environment.

Jerry Haworth is the CIO and co-Founder of 36 South Capital Advisors LLP – a leading volatility and tail risk fund manager based in London. Established in 2001, the firm specialises in finding cheap convexity, principally in long-dated options, across all asset classes. The firm’s global volatility strategies are designed to perform well in most market environments, but substantially outperform in periods of extreme market movement and volatility.

Contact: 36 South Capital Advisors LLP, Investor_relations@36south.com, TEL: +44 (0)20 3205 3004, www.36south.com

[i] Hamlet William Shakespeare [ii] Julius Caesar William Shakespeare

Related article:

Hello,

Youŕ analysis seems true, if we suppose that markets will start to wake up, i mean starting to move again.

Up to now, i have some difficulties to see what could bring back a little bit more of volatility. Except the interest yields which could bring a little bit of turmoil if they begin to rise, but majority of people doesnt see that before mid 2015.

What i mean is that this low volatility regime can continues again and again, thus buying vol even long term vol could put us to theta losses with alomost tiny gamma profit or even zero delta profit.