By Simon Kerr, Principal of Enhance Consulting

The extract below is taken from an article by Michael Langton, Head of Sales at Quality Risk Management & Operations (QRMO) Limited, that makes some interesting points. It was first published in IPAsia in January 2009. For the full article go to IP Asia or EurekaHedge. Only one sentence has been edited from the extract. The article first looks at risk management in financial institutions before turning to hedge funds specifically. The extract begins at the joint of the two parts.

What’s wrong with Risk Management?

…Continuing with this example, risk management simply becomes a regulatory-required function to senior management that should only be put in place to appease the regulators, but one that under the surface of it has no real independent authority to balance the risk/return profile for the organization. Furthermore, the far more insidious fact of the matter is that investors will think they are investing in a prudent or well-structured institution and their capital is protected by these highly paid professionals.

Hedge funds are unregulated financial pools of money provided by qualified professional investors. The rationale for the existence of this industry is that traders can utilize their special skill sets to generate absolute uncorrelated returns for its investors. However, as with financial institutions, the compensation scheme is still asymmetrical in this industry and could arguably be even worse. This is because the hedge fund manager has the discretionary right to decide whether the fund needs to have a risk management infrastructure in place. It cannot be denied that there are some well-disciplined hedge fund managers that attempt to incorporate best practice risk management and operational infrastructures through the active use of and stringent adherence to a well thought out rules-based structure. However, they tend to be exceptional cases in the hedge fund industry as a good portion of them are purely return focused instead of risk-adjusted return focused.

Some fund managers consider themselves to also be the “risk managers”. Surely, their role as a trader is the first-line risk manager as they can actively manage their portfolio and adjust the risk-return profile dynamically. However, it should be recognized that they still need to have a risk manager in place as an independent verifier that the fund manager is adhering to the risk guidelines and rules put in place. The role of an independent risk manager is not merely to provide risk measurement and reporting but to also setup the necessary risk and valuation policies & procedures and risk limit structures and to monitor the market condition changes and related market exposures of the fund.

The most important role is to execute all risk policies & procedures as stated in the offering memorandum and additional guidelines provided to the investors. Unfortunately, risk policies & procedures execution is usually ignored and not enforced. In fact, some hedge funds can have very presentable and detailed risk policies and procedures, but they are simply for showing the investor how they perform their “prudent” risk management functions. They rarely delegate the authority to the risk manager to execute actions like stop loss or position reduction if limits are breached, for example. If a fund has a risk manager but the de facto person in charge for actions taken on limit breaches is still controlled by the fund manager, the independent risk management function should be called into question. There is a lot of talk about the need for better risk management, particularly given the current state of affairs in the global world markets. However, the focus should not be on better risk measurement, although this is still important. Instead, the real focus should be on corporate governance in ensuring that a proper risk management structure is in place and that it is independent, continuously adhered to and fully transparent to the investor. In essence, corporate governance will always be the key to good risk management. As such, for the future of risk management to be successful, its function has to be directly reportable to investors instead of internal management. Such a structure should carry out these two key functions:

- Greater transparency on what the institutions/funds are investing in (esp. on derivatives) and the accurate and timely reporting of their true risk-return profiles; and

- Risk management function must be truly independent from the profit making function, so investors can truly enjoy absolute upside return from the profit maker but still have downside protection from the risk manager.

This structure will make the profit maker consider the risk elements of his strategy more carefully because they will know that the risk manager has the authority to enact his duties as per the agreed risk policies and procedures. Ultimately, risk management should no longer be viewed as a “regulatory-required” function but as a “value-added” function in the investment decision-making process. The “value-added” does not derive from making money, but rather from capital preservation, particularly in down markets.

Experience, discipline, communication and common sense are always the essential elements of a good risk manager. Some market participants misunderstand that having expert quantitative staff and a sophisticated risk system is sufficient. This misperception stems from a false sense of comfort that can come from the risk managers’ utilization of a lot of different mathematical models (e.g. VaR, Monte Carlo, auto-regression, scenario analysis, etc.) through the use of expensive state-of-the-art technology to assist the risk manager’s decision process. However, these quantitative elements and technologies are not the only factors needed to determine whether the organization has a robust and proper risk function. More importantly, an experienced risk manager needs to effectively communicate with the profit makers and understand the risk and return of each product/portfolio while also demonstrating these risks to senior management and investors.

In summary, inevitably regulation will always be tightened post-crisis, which will, in turn, prompt the need for more robust risk management to avoid crises from happening again. However, this time, regulators and investors should consider demanding changes at the highest levels of the corporate governance structure. These changes will need to grant the risk manager a more independent role which can directly report to investors (especially within the hedge fund industry), so that risk management can play a more pro-active role. It goes without saying high quality risk managers that have a better understanding of risk will also be a key to successful risk management. Importantly, sophisticated risk systems and quantitative models are not the only components of a solid risk function. In some cases, good old common sense will be a better suited method to justify particular actions to a given situation. (end of extract)

From Simon Kerr:

I have enjoyed a privileged position over my 11 years in the hedge fund industry. From 1996 when I attended my first hedge fund conference in London (there were 5 paying attendees, way out-numbered by speakers), I have met many first-rate hedge fund managers. I now apply the insights they have given me in my consulting work, and in my own investments. One conclusion I have reached from meeting first-tier managers is that the very best hedge fund managers have a keen appreciated of risk management. An understanding of what risks they are currently running and how those risks might change, subject to market dynamics, is a core competency for them. The kind of preparation for the trading day undertaken by the likes of Paul Tudor Jones and Steve Cohen is one of the reasons for their successes, and both include elements of risk assessment as part of their preparation for battle. They get/produce relevant risk information for their style, they think through various scenarios that can happen to their exposures, and they plan responses. A good local example is Lee Robinson of Trafalgar Asset Managers in London.

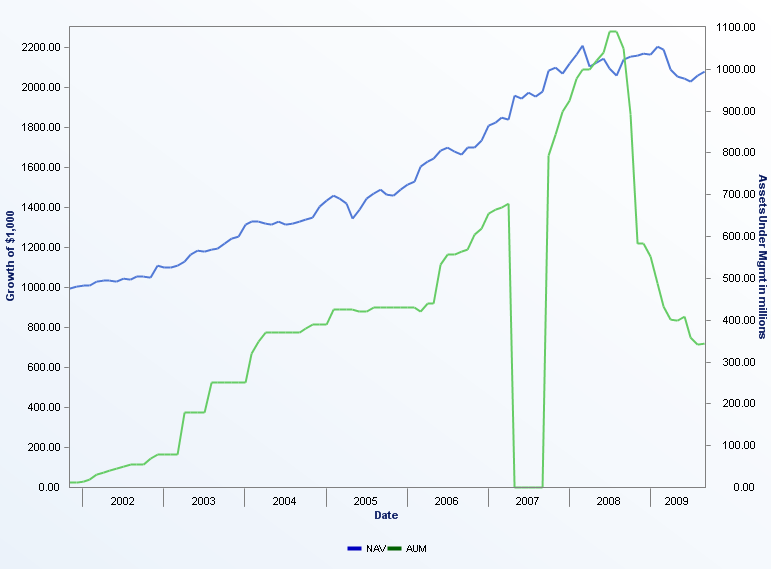

Robinson’s view is that market crises in reality happen with a greater frequency than generally perceived. “Markets have had serious moves almost every year this Millennium,” he has said. As a consequence Robinson has disclosed that the bulk of their work on a trade at Trafalgar is preparation. “We are prepared for the worst,” was how he summed up the rehearsal of various possibilities (mark-to-market difficulties, drawdowns, shifts in volatility, and redemptions) that might be experienced en route to the planned exit points. He said that the aim is not just to avoid losing money, but to avoid the forced liquidation of positions. He has succeeded in that aim: the graphic below reflects that his event-driven Trafalgar Catalyst Fund made absolute returns of 4.83% last year. Since inception the Trafalgar Catalyst Fund has compounded at 9.7% (in the USD Class) versus 2.2% for the HFN event Driven Index over the same period.

NAV of the Trafalgar Catalyst Fund (USD)since inception

Lee Robinson has made a conference speech titled “Lessons from the Crisis”. He made it in November of 2007 (not 2008 or 2009!), so he was ready for the unfolding crisis from having seen warning signs in the previous few months of 2007. In his presentation he talked about portfolio management. He stated that it was easy to have investment ideas, but difficult to mesh together those ideas into a coherent portfolio, and even harder to make that portfolio robust to varying market conditions. He cautioned that investors in hedge funds should look closely at funds that exhibited high weekly and monthly correlations, and to beware of funds that had high concentrations of risk. Robinson continued that all portfolios are essentially short liquidity and at risk to mark-to-market movements, but that all great portfolio managers have tools to combat these problems. Robinson suggested that carrying long put option positions below spot which defines the downside more clearly, and being short interest rates and short credit will all help, or if you like, are examples of such tools. Lee Robinson concluded that “The best managers are not the ones with defined upside and a wide range of possible downside outcomes. They are the ones with defined downside and a wide range of upside.”

Lee Robinson has made a conference speech titled “Lessons from the Crisis”. He made it in November of 2007 (not 2008 or 2009!), so he was ready for the unfolding crisis from having seen warning signs in the previous few months of 2007. In his presentation he talked about portfolio management. He stated that it was easy to have investment ideas, but difficult to mesh together those ideas into a coherent portfolio, and even harder to make that portfolio robust to varying market conditions. He cautioned that investors in hedge funds should look closely at funds that exhibited high weekly and monthly correlations, and to beware of funds that had high concentrations of risk. Robinson continued that all portfolios are essentially short liquidity and at risk to mark-to-market movements, but that all great portfolio managers have tools to combat these problems. Robinson suggested that carrying long put option positions below spot which defines the downside more clearly, and being short interest rates and short credit will all help, or if you like, are examples of such tools. Lee Robinson concluded that “The best managers are not the ones with defined upside and a wide range of possible downside outcomes. They are the ones with defined downside and a wide range of upside.”

Whilst the tools Lee Robinson suggested may be specific to his event-driven strategy, a more widely applicable point can be made: portfolio construction has to take account of the possible outcomes for the asset class/specific securities including downside and liquidity risks, and particularly tail-risk. The best hedge fund managers manage whole portfolios not just select securities or investment themes they like (longs) and dislike (shorts).

My second major point is that risk managers work best when they work with and alongside portfolio managers. This applies whether in a long-only firm, a hedge fund management company or some combination. Several good examples come to mind. At Augustus Asset Management, the fixed income specialist part owned by GAM, Risk Manager Amy Kam sits in with the portfolio managers and is part of general discussion on trading strategies and the dialogue on portfolio level risk and rates. Augustus uses stress-testing, simulations (Monte Carlo), and sensitivity analysis in the arsenal of risk assessment tools. The risk control framework goes beyond the managers’ spreadsheets and is externally supported (by Riskmetrics) and working with GAM’s wider risk analysis capabilities.

The physical location of the risk manager in the office suite is indicative of their hierarchical position in the firm and their level of significance to the portfolio managers. It is one reason why, even on a brief visit to see a manager, a look at the trading room is always useful. An example of this is Charlemagne Capital in St.James’s London. The office space is a little tight so it would be all too easy to place the risk manager in a room adjacent to the analysts and PMs. But at Charlemagne the risk manager is too integral to the investment process for him to be squeezed away from the hub of investment activity. The risk manager at Charlemagne Capital works with the portfolio managers day to day on their portfolio construction challenges and not just reporting to investment team heads Julian Mayo and Gabor Sityani once a week.

The final point is that risk management is most effective when it is an element of the investment culture rather than a segregated function. Too often the risk manager can be seen as part of the oversight of fund management activity rather a core element within it. The risk manager as part of compliance or as a policeman looking for infringements of policy may be useful for marketing purposes but is unlikely to play well with the star portfolio manager. There is a chance that the risk manager will be seen as having no relevance to the men and women running the money. This quasi-regulatory attitude and structure is very limiting and indeed isolating for the risk manager. The senior management of the asset management businesses whether hedge or long-only can do something about these potential difficulties by recruiting a risk manager with the right attributes – they should be bright, open, engaged with markets, experienced, have good judgement, and be both quantitatively capable and have good people skills.

This is a long and demanding list of characteristics, and perhaps its length makes clear how difficult it is to find the right person for these roles. The attributes are also those of the best hedge fund managers – which is why the hedge fund managers are often also their own risk managers!