By Twelve Capital

Insurance Bonds

For the Insurance Bond market, the year started with fears of European wide deflation and sluggish growth across the region. This spurred the ECB to act decisively and initiate a programme of quantitative easing which it intended to last until 2016, pumping EUR 60bn a month into the market.

The swift reversal in yields in mid-April caused significant volatility across broader markets, and a number of factors have been attributed to triggering this sell-off. Whilst the Eurozone experienced an upward tick in GDP, there was also, and perhaps most importantly, a strong technical bias across the market as investors positioned themselves for a flattening yield curve in Germany.

Just as one bout of volatility passed, the markets were again immersed in the economic storm clouds of Greece. Towards the end of the first half of the year, there was the hope that Greece would be able to renegotiate terms with its lenders, the assumption being that Prime Minister Alexis Tsipras would bow to pressure from the European Council, ECB, IMF and others in order to maintain Greece’s status as a member of the European Economic and Monetary Union. However, on 25 June, Tsipras announced that he intended to call a referendum on the final EU bailout offer, a referendum which resulted in a resounding “no” vote from the Greek people. This new chapter has left open a whole series of technical questions on what a Greek exit would mean for Europe and its lenders.

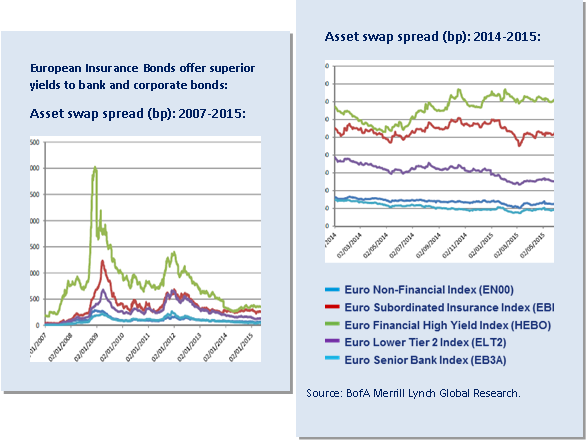

Despite these negative headlines and unquantifiable risks, the market has demonstrated some resilience compared to the last time similar concerns around Greece were raised in 2011 and 2012. Insurance Bonds have come under pressure, as have all sectors, not only from the volatility caused by underlying government markets but also from a general lack of liquidity. In addition, the first half of the year saw the market flooded with new issuance from corporates, most notably in the Financials space, of which approximately EUR 11.4bn of new issuance was in European insurance. This has had a strong short term negative effect on markets as investors struggled to recycle risk given the lack of liquidity across all asset classes. The effect of such a situation has created some compelling opportunities within the insurance sector. The average subordinated insurance bond now yields between 4.75% and 5.5% on a relative value basis (compared to European bank lower Tier II debt at 3.0% for instance). We have been taking advantage of such market dislocation and adding risk across a wide variety of names.

Private Debt

In the Private Debt space, the first half of 2015 was characterised by a reduced number of transactions. Back in January, potential issuers held back planned debt issuances in order to await the outcome of negotiations with Greece, which were at that time supposed to come to a conclusion. As those negotiations dragged on, prospect issuers became more vocal about their willingness to issue debt. While liquid Tier II instruments corrected from late April, Private Debt proved to be a stabiliser in the portfolio. On the liquid side, a sharp upward correction in underlying government yields, as previously mentioned, as well as concerns regarding expectations for US based issuers to call their bonds at the first call date, were the main reasons for pricing pressure on larger benchmark issues.

With the Solvency II deadline of January 2016 approaching quickly, the requirement to issue compliant debt this year, on both the private and the public side, is increasing. As per the end of Q2, Twelve Capital were aware of 20 deals in the pipeline (both from Europe and the US) at various stages of development. Given the recent spread widening in liquid markets for subordinated insurance debt, we also anticipate that spreads for those smaller issues will move up – a positive prospect for the remainder of the year.

It is also worth noting a recent uptick in the number of US Private Debt transactions in the pipeline. This is due to: i) the tendency for companies to borrow in the second half to facilitate funding requirements for the following year; ii) maturing of the more successful Florida based insurers to develop multi-state strategies; and, iii) burgeoning development of a domestic market in Louisiana, resulting from recent legislative changes.

Catastrophe Bonds

There has been around USD 5bn in volume of newly issued Cat Bonds split between more than 20 tranches placed in the market in the first half of 2015. Innovation, driving the development and growth of the Cat Bond space, was seen affecting both trigger types and the wide spectrum of territories covered – transactions varied from parametric matrix US hurricane coverage to Italian earthquake risk. The convergence between traditional reinsurance and Cat Bonds was further enhanced with the introduction of risks such as volcano eruption.

Average coupon at issuance for 1H 2015 was around 5.3% and the respective expected loss amounted to around 2.2%. Spreads widened on the secondary market as a result of a healthy pipeline of primary issuance, combined with the decay of excess institutional capital within the market. We continued facilitating the issuance of Private Cat Bond transactions, which in turn helped us improve diversification, achieve attractive risk-adjusted returns and benefitted our clients with faster and more efficient utilisation of capital. The potential average return to investors of these transactions is expected to exceed 7% annually.

Issuance activity is anticipated to remain strong in the second half of the year, with the majority of Cat Bonds expected to be marketed during the fourth quarter (post the hurricane season). We expect that total issuance by year end will be at least USD 7bn for publicly offered Cat Bonds. We expect continued expansion of the overall Private Cat Bond universe, both in terms of issuance and covered perils/risks and we will continue our efforts with the origination and execution of the Dodeka Series (Twelve Capital’s own sourced and structured Private Cat Bonds).

On the weather front, we anticipate the Atlantic hurricane season activity to be below average, mainly due to the aforementioned El Niño and the current rather low sea-surface temperature. We anticipate a mark-to-market price rally for Cat Bonds exposed to US hurricane risks during the July to September months. This is a standard pattern derived from seasonality, yet it is expected to be stronger this year as the Cat Bond market becomes more efficient. In terms of pricing dynamics, we do not anticipate a decline in rates on a risk-adjusted basis until year end, provided no severe natural hazards materialise.

Private Insurance-Linked Securities

Private ILS taps into a variety of (re)insurance opportunities that are continuing to generate returns in excess of comparable Cat Bond securities. As these contracts generally offer 12 month protection to buyers, the premium earned above the return for traditional Cat Bonds is, to a large extent, due to the illiquid nature of the investments. This sub asset class provides a broad degree of diversification to ILS portfolios, resulting in exposure to harder to find natural peril regions, such as Australia or Europe, as well as access to man-made perils such as marine and fire.

In the Private ILS market, renewing a large part of our portfolios in January proved to be a wise strategic decision as, over the course of the last six months, there has been a continuation of spread erosion within the space. Yet, throughout the first half of 2015, capital markets reflected their pricing discipline by rejecting a number of Cat Bond issuances with less than favourable risk/return characteristics. This is often the first sign of a turn-around in the underlying reinsurance space and, at the time of writing, prices for industry loss warranties (ILWs) have stopped retreating, with some levels starting to improve.

We are positive on the Private ILS market over the second half of 2015, but not without reason. The ILS space has been shown to be a very sophisticated market, keen to collect the right premium over risk and continuing to use complex mathematical modelling to ensure pricing remains appropriate and that margins are not eroded. We expect to see a firmer market in the next six months of the year and, even without a significant event, believe that despite some suggestions of pricing declines, the next round of renewals will likely see pricing stabilisation within the Private ILS space.

Investment Conclusions

Solvency II is likely to be the key fundamental issue that will impact insurance debt and equity investor sentiment over the remainder of 2015, driving asset value ambiguity and creating compelling investment opportunities.

Within the Insurance Bonds space, although recently under pressure with the rest of the market (due to the volatility caused by Greece’s sovereign debt travails, a general lack of liquidity and significant amounts of new issuance), the effect of such a situation has created some compelling opportunities within the sector. In Private Debt, the Solvency II deadline of January 2016 is fast approaching and given the spread widening experienced in liquid markets for subordinated insurance debt, we anticipate a similar widening amongst the smaller issuers, a positive prospect for the remainder of the year.

Due to innovation and the introduction of new cedants and trigger types, Cat Bonds will continue to offer solid diversification opportunities throughout the remainder of the year, both relative to mainstream financial markets and also internally within the space (given the lack of correlation between relevant risk categories). Spreads will be stable and continue offering strong risk-adjusted returns to investors. Furthermore, we are positive on the Private ILS market over the second half of 2015 as pricing remains rational and margins attractive. We expect to see a firmer market in the next six months of the year and, even without a significant event, believe that the next round of renewals may see stable pricing levels.

About Twelve Capital

Twelve Capital is an independent investment manager specialising in insurance-related investments, which include: Insurance Bonds (instruments issued by insurance companies for regulatory capital purposes); insurance company Private Debt (issuances by smaller insurers with strong balance sheets); Catastrophe Bonds (bonds covering the risk of defined insurance events – such as earthquakes and hurricanes) and Private Insurance-Linked Securities (which provide exposure to a broader range of insurance risks, such as crop risk, fire or terrorism).