By Manuel Arrivé and Alastair Sewell of Fitch Ratings

Faster Industry Changes Ahead: Fitch Ratings’ view is that the European asset management industry is ripe for faster change and possibly disruption. As an industry that has historically been slow and reluctant to change, asset managers show varying degrees of willingness and ability to adapt but the status quo is no longer an option as institutional investors’ standards continue to rise.

Lower AUM Growth Expected: The European asset management industry grew by another 10% in 2015 to reach an all-time high at the end of last year. Fitch expects more moderate growth in 2016, assuming lower systematic market returns and decelerating inflows.

Industry Under Scrutiny: European asset managers (AMs) are under intensifying scrutiny from regulators and investors. Specifically, active AMs are under pressure to justify in a transparent manner their returns relative to fees charged given lower market returns and the continued shift to low-cost, passive investments.

High Margins Threatened: New decelerating AUM growth adds to the pressures on pricing that is weighing on European margins in 2016. Fitch expects management of AM companies to take bolder restructuring or strategic decisions to protect profitability and corporate resilience.

Shifting Business Mix: The shift to outcome-oriented, client-centric solutions from performance-oriented, product-centric approaches is a secular trend in the industry. A related trend is the fast growth of alternative investments, particularly real assets. AMs are enhancing their capabilities in these sustainable growth areas but those that positioned themselves early are benefiting from a key competitive advantage.

More Efficient Operating Models: Increasing the efficiency of operational platforms is on the agenda of AMs looking to re-invest profits. More flexible operating models are necessary to reduce costs, keep pace with rapid technological shifts and deliver increasingly tailored and/or a broader service proposition to clients in a scalable manner.

Disruptive Trends Force Innovation: Data and technology are becoming strategic assets for investment managers, due to their potential for providing new sources of alpha generation and asset raising. AMs recognise that digitalisation and a more systematic use of data analytics can enhance client servicing and sales capabilities.

AUM and Flows Slowdown Expected

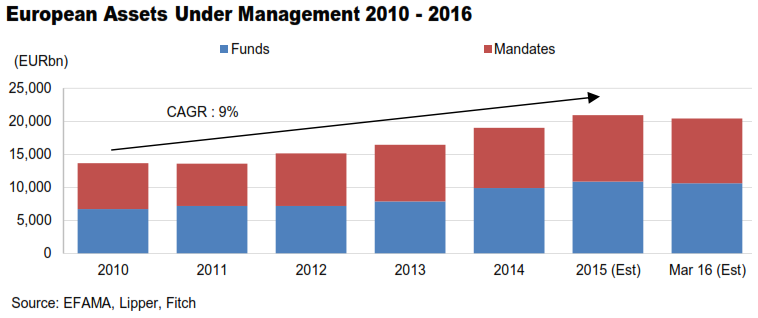

End-2015 AUM At All-Time High: The European asset management industry grew by another 10% in 2015 (see chart below), which is in line with its compound annual growth rate of 9% over the last five years but lower than the estimated growth in the US and East Asia (respectively 11% and 16%). Overall, the industry has almost doubled its size since 2008. The increase in AUM in 2015 was driven by net new assets, the largest inflows since 2007, rather than asset performance.

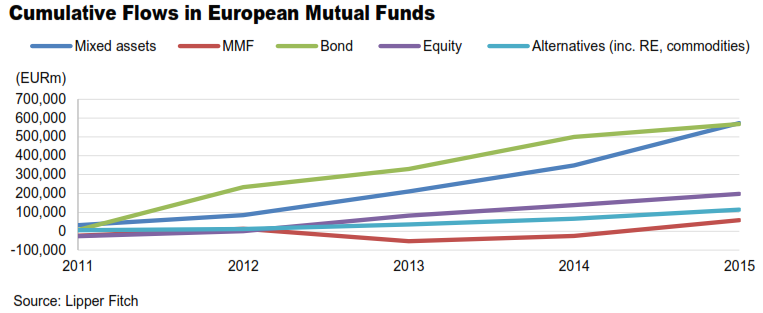

Flow Reversal in 1Q16: All major aggregate fund types recorded inflows in 2015, as QE drove asset rotation, including money market funds, despite negative yields (see chart below). Multiasset funds drove around 50% of industry-wide net inflows in 2015. Flows into fixed income slowed considerably, with EM and US High Yield bond funds suffering from net outflows.

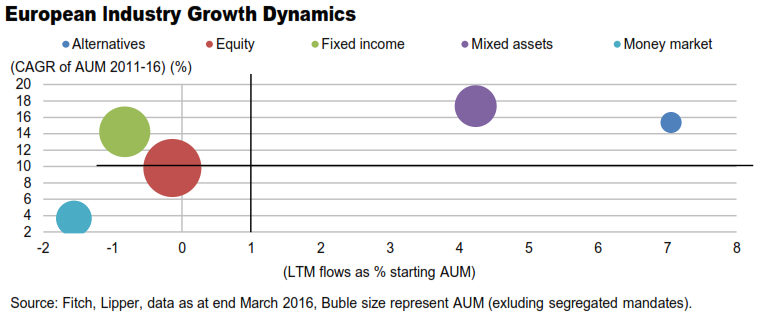

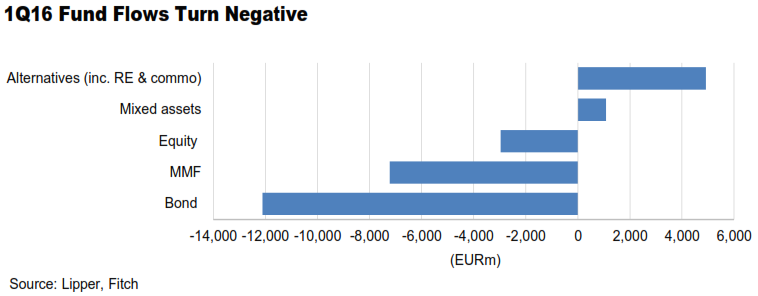

This reversed in 1Q16 when most major asset classes recorded outflows, with significant redemptions from bond funds (see chart above). By contrast, investors raised allocations to alternatives, in search of returns that are less affected by market cycles.

Lower AUM Growth Expected: 2016 may mark an inflection point for industry growth. Fitch expects AUM growth to moderate, as a result of lower systematic market returns and decelerating inflows from sovereign wealth funds and retail investors. Flow dynamics vary widely by asset class and therefore do not affect AMs evenly. Multi-capability players are less exposed to asset rotation risk than specialist players (e.g. specialist EM managers in 2015).

Resilient Growth Drivers: Multi-asset solutions and alternatives should continue to be the main strategic priorities to drive growth in actively managed funds. Segregated institutional mandates (in fixed income, multi-assets and alternatives – see paragraph on competition and demand) and cross-border retail flagship funds should continue to be recipients of sustained inflows in 2016 (see chart below).

Pressure on Margins for Strategic Initiatives

Eroding Margins: Deceleration in AUM growth will weigh on earnings growth in 2016. The revenue margins for European AMs have declined since 2010 as a result of fee pressure and shifts to lower margin products and client mix. Regulatory, compliance and litigation costs have increased as have asset gathering/retention costs. Fitch expects AMs to take new measures to withstand pricing and cost pressures to maintain profitability.

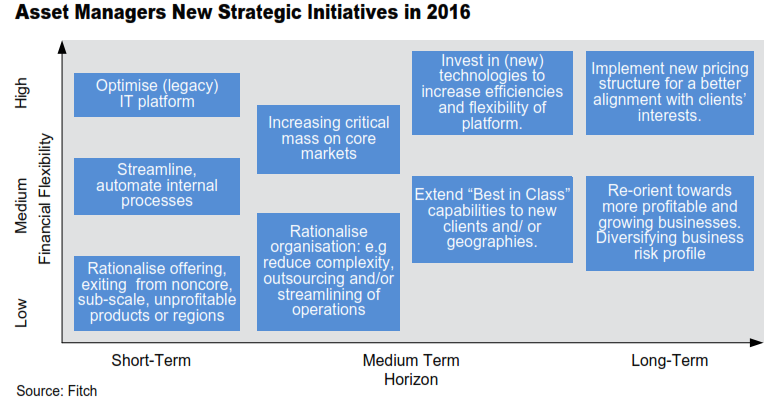

New Restructuring/Strategic Initiatives: European AMs are working on increasing operational efficiency to reduce costs, while using financial strength to re-invest for future growth. AMs that shifted early their business positioning in anticipation of the next investment cycle or emergence of long-term, sustainable growth areas have developed a key competitive advantage.

Fitch expects managers to increase the efficiency and flexibility of their operational platforms. AMs with lower break-even points and/or a longer-term strategic focus can take bolder actions, either through organic or external growth (acquisition, team lift-out, partnerships) (see chart below).

Competition and Demand: Secular Trends Intensify

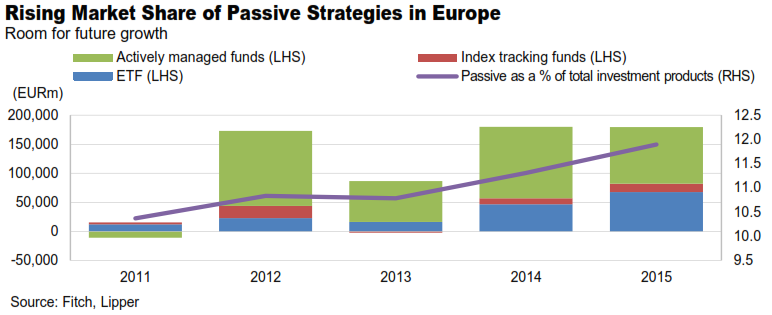

Shift to Passive Continues: Investors’ demand for low-cost, transparent, liquid products has driven the growth in passive strategies since 2009. The market share of ETFs and index tracking funds has risen consistently as a result of inflows (see chart below). There is still room for growth, particularly in fixed income, as ETFs and passive funds only represent 12% of the total of investment products domiciled in Europe (versus 23% in the US).

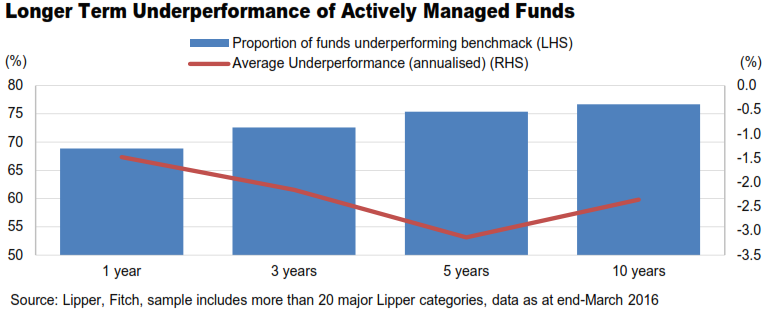

The difficulties that actively managed funds face in outperforming their stated benchmarks (i.e. equivalent passive strategy), net of fees1 have accelerated the shift towards passive strategies (chart below).

Active Management Fights Back: Lower systematic returns (beta), higher idiosyncratic risk, and global desynchronization may support active management performance2 , which has improved over the past 12 months. AMs have been encouraged to demonstrate their active management skills3, as European regulators and groups of investors increase scrutiny on value for money. The rise of passive funds also represents an opportunity for active AMs who use ETFs as a component of cost-efficient beta strategies or, more broadly, outcome-oriented solutions, which have been a driver of ETF growth in Europe.

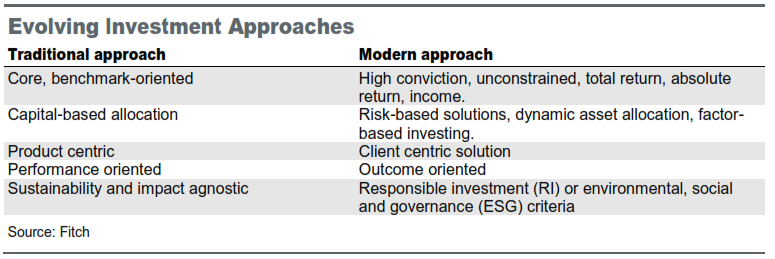

Outcome-, Client-Oriented Solutions: Traditional investment strategies are brought into question by secular investor demand and market trends, which favour more client-centric and solution-oriented approaches (see table below). The trend provides an opportunity for AMs to play a broader role in the industry’s value chain beyond t he pure generation of risk-adjusted return, by providing innovative retirement solutions, for example.

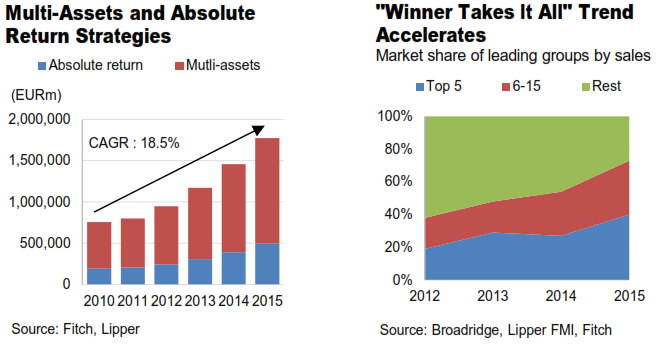

European AMs therefore are further investing in client-solution capabilities in key areas such as pensions. Multi-asset and absolute return investments benefit from the strong demand in goal based solutions, growing at a faster rate than the industry average (see chart on left) – a trend that is more pronounced in Europe than in the US.

European AMs therefore are further investing in client-solution capabilities in key areas such as pensions. Multi-asset and absolute return investments benefit from the strong demand in goal based solutions, growing at a faster rate than the industry average (see chart on left) – a trend that is more pronounced in Europe than in the US.

Real Assets in Demand: Long-term institutional investors are moving down the liquidity spectrum, increasing allocations to real assets. Private-market exposures (mortgages, private placements, infrastructure (debt and equity), private equity, real estate, renewable energy) gain in popularity, as the benefits of incremental yield and diversification outweigh the obstacles of low accessibility (non UCITs structures), illiquidity and regulatory restrictions.

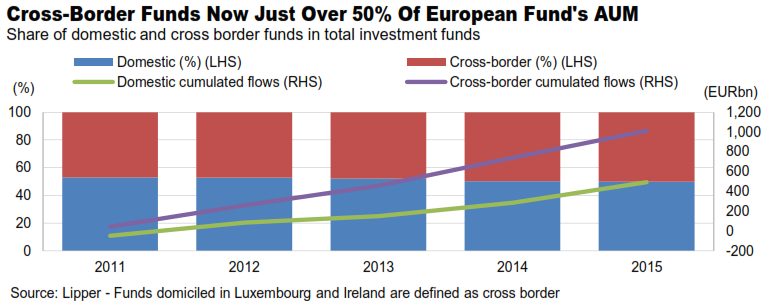

“Winner Takes It All”: The phenomenon is accelerating in Europe (see chart bottom left). Yet, as in the past, superior returns alone do not drive flows, as clients value service. The trend is consistent with that of a European market that is becoming more integrated, with a post-crisis concentration of institutional investors, intermediaries, and fund selectors.

New Disruptive Trends Force Innovation

Business Digitalisation: AMs are embracing digitalisation to respond to rapidly changing investor needs in services and interfaces. It is expected that digitalisation, coupled with a more systematic use of data analytics for client profiling and market intelligence, will enhance client servicing and sales capabilities. Digitalisation has the potential to make asset management more accessible to retail investors and smaller institutions, thereby contributing to democratisation and potentially disintermediation of asset management. In the short to medium term, fintechs and other new entrants to the broad industry are more likely to represent a threat to wealth managers and intermediaries than asset managers, in Fitch’s opinion.

Data Science Applied: Some leading AMs have invested in experimental big data technology to enhance research and decision making. Data units, staffed with sought-after data scientists, work on harnessing large datasets (tweets, blogs, broker research, social media) and developing advanced predictive models.

Technological Edge: Data and technology are becoming strategic assets for investment managers, as they have the potential to provide new sources of alpha and asset raising. However, this advantage may not be sustainable if it is threatened by rapid technological evolution, duplication or cyber-attacks.

R&D in New Alpha Sources: AMs place a more rigorous focus on investment research and innovation, as traditional investment strategies become less efficient in an environment of lower returns, higher correlation and higher volatility. Current R&D efforts at AMs focus on risk premia engineering (factor-based strategies, dynamic risk premia allocations) and efficient portfolio construction techniques (trading strategies, drawdown management, option-based strategies

for convexity).

Shifting Staff Competencies: Asset managers have to adapt their staff competencies to industry evolution. On the investment side, Fitch doesn’t expect major changes in the core required investment skills but competencies in alternative strategies will be increasingly sought after. The increased automation of investment processes is already leading to staff reductions in certain areas of the production chain, such as equity trading. Conversely, technological and data expertise are increasingly sought after throughout the organisations.

1 Data show that indices are harder to beat either in the least efficient markets (such as emerging market

debt, for liquidity and transaction cost reasons) or in the most efficient markets (such as US equities).

2 Performance is driven by a combination of alpha (manager skills) and beta (market-driven returns).

3 Investors would view positively a disclosure of active share and charges, for instance.