From Keith Haydon and Adam Singleton of Man FRM, part of Man Group

![]()

- Markets return to an uneasy calm in July with rising equity markets and falling volatility.

- Commentators continue to watch the shape of the US yield curve for clues.

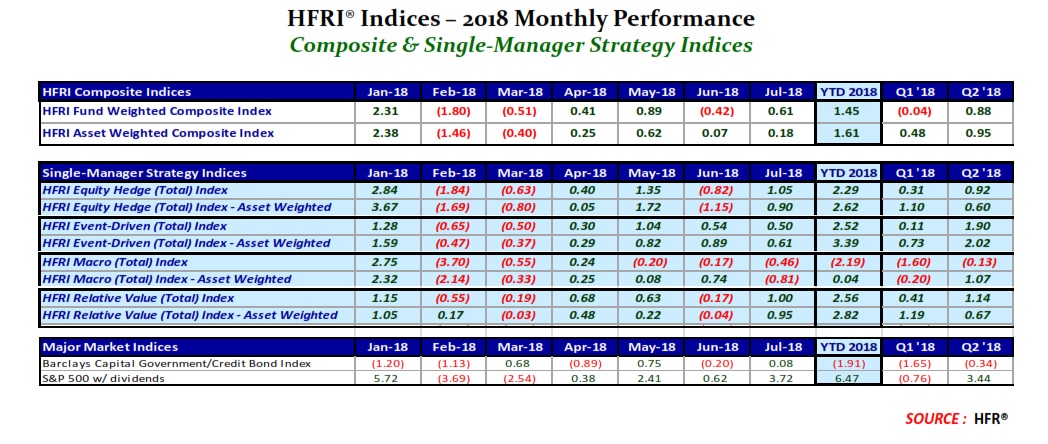

July continued the difficult year for hedge fund performance, with mixed performance across strategies (as has so often been the case in 2018). On the whole, risk asset strategies in equities and credit performed better, helped by a strong earnings season and generally rising markets. Relative Value struggled, due to a hangover from the quantitative market neutral sell-off in late June and the underperformance of Event Arbitrage strategies around high profile deal breaks. Macro strategies were generally mixed, as markets reversed some of their June moves which hurt some trend following strategies.

Starting with equities, as expected, managers with higher equity market net exposure generally did better in July as markets rose, with US exposure proving to be the most fruitful. Managers are generally slightly more bullish than they have been for some time, supported by the apparent resilience of macro data and corporate earnings twinned with the fact that the general risk reduction environment of the first six months of the year means that some of the ‘fast money’ from markets may have been flushed out already. Alpha generation in non-directional managers was muted but generally positive, again supported by the earnings season. A notable detractor on the month was a social network company, which is well held by the hedge fund community and whose shares plunged after missing top-line estimates.

In a risk on month supported by improved sentiment, global credit markets rallied alongside of equities while US treasury yields were higher. Notably, after lagging for the past two months, EM and European credit markets posted healthy returns. US investment grade credit also showed some strength after underperforming for most part of the year. New issuance in US high yield continued to be driven by a decline in refinancing activity leading to one of the slowest months in the last five years. Corporate Credit managers were generally positive in the month but returns were more modest compared to June with few meaningful single name performance drivers. Several distressed credits and equity reorg names that had positive idiosyncratic news in June continued to see positive momentum. Managers with larger reorg/value equities exposure outperformed. Credit shorts were a drag on performance.

In Structured Credit, it was another month of relatively muted price moves with spreads stable across most securitized products sectors. Private student loans saw some renewed interest as there was a large block that traded on a bid list and there were a number of other secondary trades. Otherwise trading activity was light in the month. Corporate and CMBX hedges were a drag on performance for some managers. Overall, it was another month that was largely driven by principal and interest income.

During the month, risk arbitrage had mixed performance. Overall, deals are progressing at a healthy pace towards completion and the pipeline of new deals remains robust. Vertical integrated deals and cross border deals remained the focus of attention during the month. In vertical integrated deals, the bidding war for a media company ended with one bidder (a telecommunications company) dropping its offer and focusing on purchasing a newscaster company instead. Sector focus has now shifted on whether another bidder (a media company) will top the telecomm company’s offer for the newscaster especially after the company reported attractive sales and subscription numbers during the last week of July.

A telecommunications equipment company/a global semiconductor manufacturer deal break was a notable detractor across the sector during the month of June. The former walked away from its bid to acquire the latter as the Chinese regulators failed to give their sign off given the mounting trade tensions between the US and China. As a result, the semiconductor company sold off and managers across the sector reduced exposure.

In Statistical Arbitrage, returns have stabilized after a difficult June, but haven’t rebounded as strongly as we have seen in previous dislocations. However, there was a danger that the poor performance in June might have led to a run on the more liquid products trading quantitative equity market neutral strategies, which in turn could have led to deleveraging, which it appears has not happened. More broadly managers in this strategy continue to find it difficult to add value while stock specific volatility remains so low. It may be a natural output of the fact that investors are increasingly accessing markets through passive or factor based products, rather than active managers, therefore most of the flow impact on markets is leading to market or factor volatility, rather than single stock volatility (as would be the case with higher volumes of active management).

CTA managers saw gains in equities as they tend to still hold long exposure to the asset class. Most other asset classes lost money in July. The main differentiator between the better and worse performing managers was the speed that they were able to reenter and build up US equity positions into the rally. Across the board managers are still close to maximum levels of short FX exposure (versus a long dollar position), which detracted from performance during the last third of the month as the dollar softened.

related content: