By Douglas Garistina Chief Executive Officer of Sequoia Capital Fund Management

![]() ‘What is a favourable environment for my strategy’ is a question that every portfolio manager must be able to understand and identify. The answers will, of course, depend on what type of strategy is being run, the markets the strategy focuses on, its holding period, volatility characteristics and various other factors. And while we should all be able to compose a clear definition of what constitutes a favourable environment for our particular strategies, it becomes considerably more challenging to propose that the future will entail such a favourable environment.

‘What is a favourable environment for my strategy’ is a question that every portfolio manager must be able to understand and identify. The answers will, of course, depend on what type of strategy is being run, the markets the strategy focuses on, its holding period, volatility characteristics and various other factors. And while we should all be able to compose a clear definition of what constitutes a favourable environment for our particular strategies, it becomes considerably more challenging to propose that the future will entail such a favourable environment.

At Sequoia Capital Fund Management LLP, we run quantitative, systematically-driven strategies. Our focus is on short-term opportunities that exist for a few hours to a few days as this is where we see genuine Alpha opportunities existing. The models that we develop are tested over several years of out-of-sample data to build an empirically derived picture of their performance characteristics through many different trading environments with a reasonable level of granularity.

By running a quantitative, systematic strategy we are able to identify and capture statistically meaningful and repeatable Alpha events. The discretion and emotion are taken out of the equation and we can clearly identify market environments when the signalling in the market was coherent and beneficial to the performance of the strategy and when it was not. Then, providing that the underlying theory of the strategy is sound, we can expect a systematic strategy to perform within certain statistical bounds. Of course, the future is always an incomplete equation and therefore there is only a certain degree of precision with which we can extrapolate our empirical findings.

Before we address the question of what is a favourable environment for our strategy, we really need to define the strategy and its purpose, and to do this I think it best to ask ourselves a series of preliminary questions about why we do what we do:

Why do we think an exploitable trading opportunity exists?

Why might the markets exhibit a certain behaviour?

Why should our method of illuminating this behaviour or opportunity be profitable?

Why should an investor want a product like ours to diversify his/her portfolio?

At its most basic, our primary strategy is designed to exploit the fundamental relationship between movements in interest rates and flows in/out of a set universe of liquid currencies. The many different players who focus on global markets (currencies, interest rates and equities) respond to the incentives of investing in one country or another by following economic figures, policy statements, sentiment surveys, etc. and create flows in these asset classes based on rational assessments of this data. While there isn’t solely a one-way causality between the movements of these different asset classes, the supply and demand flows in each of these asset classes lead to expected outcomes in the others. And while the relationships are not as tight as they would have us suppose in Economics classes due to the many other drivers of the markets, these relationships must exist beneath the noise and therefore should be exploitable with the application of the right tools.

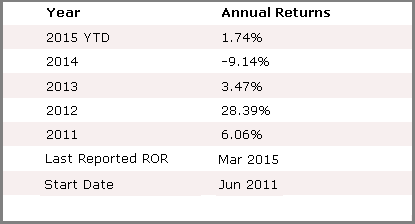

The tools and the strategy we have built have the ability to extract Alpha from the G10 currency markets to produce an average annual Information Ratio of 2.0 over the past 12 years, during which the markets have seen very different environments. By identifying these repeatable Alpha opportunities and developing a way of trading this basket of currencies efficiently to deliver this potential long-term performance, we have created a very diversifying returns stream for our investors’ portfolios.

In designing this strategy, we explicitly avoid delivering alternative beta, carry, risk premia collection as well as other characteristics that replicate the major elements of a balanced portfolio. Our strategy delivers real Alpha performance that is non-correlated to any of the major benchmarks. Our focus on delivering a high-quality product and experience for our investors has earned us multiple awards for providing the best short-term FX and derivative investment management based in the UK.

So, what is a favourable environment for our strategy and why are we excited about the future?

A Favourable Environment

A basic premise for most strategies is that the markets are freely-moving and not subject to government intervention through active manipulation or market-distorting policies. Unfortunately, during certain periods such intervention is endemic in our markets, whether it entails capping the Swiss Franc, as the SNB attempted for three years, or the multi-year asset buying of Fed QE, or even the de facto liquidity tightening that tapering causes, not to mention short-selling restrictions and plain vanilla jaw-boning to bully the markets to do what the policy makers want. Though these distortions serve to suppress some of the relationships and their signalling in the markets, over the longer term the sound relationships that underlie a good strategy must come to bear on the markets.

And so it is with interest rate, equity and currency markets and the relationships that our strategy exploits. This brings us to favourable condition one; there is less government heavy-handedness in the markets now than there was over the past couple of years. True, Europe just embarked on its own QE, albeit on a smaller scale than the US. And Greece and the UK election can cause noise and distortion (there will always be a crisis and elections somewhere though) that has the potential to overwhelm the signals in the daily data. But, importantly, we no longer have the Fed playing its massive version of QE and the Swiss National Bank is no longer attempting to single-handedly prop up the Euro by buying vast quantities on a daily basis. So while Euro QE and the negative interest rates caused by this belated policy are clearly supressing normal market signals in Europe, other distortions have lessened and in our view, on balance, this bodes well for the markets.

Volatility has returned to some of the markets (certainly to the FX markets that we focus on) as shown in the DB CVIX (Deutsche Bank FX Volatility Index) chart below.

(source: Bloomberg)

(source: Bloomberg)

Unless a strategy relies on premium collection, a certain amount of uncertainty and movement is needed in the markets to provide signals about participants’ intentions and expectations such that the signals can be heard above the noise. Without volatility, we also see a decline in liquidity which can amplify the noise in the absence of clear signals. It goes without saying that without market movement, there can be no profit (other than the aforementioned premium collection). So, volatility is generally conducive to a favourable environment. Thankfully, most central bankers have come to this conclusion over the past 6-9 months and have been purposely fomenting a return of uncertainty and thus volatility by reducing their forward guidance and giving alternatively hawkish and dovish views at different speaking events. Bank of Canada Governor Poloz wrote an excellent discussion paper in July 2014 on this topic (http://www.bankofcanada.ca/2014/10/discussion-paper-2014-6/), which I’m sure his counterparts have read. There are other causes of volatility such as from the collapse in oil prices, the removal of the Swiss cap and the Greek crisis although arguably these types of events do not deliver longer-term healthy volatility. Again, on balance, the return of volatility bodes well for the markets and our strategy has taken notice.

Favourable conditions three and four: The G10 economies are diverging and Central Banks are talking about normalising their interest rate policy making. After years of countries working together through the aftermath of the financial crisis by providing open taps of liquidity and lending to banks, we are finally seeing different stories coming out of different countries depending on the policy courses they each followed and their respective economies’ responses. This must spell opportunity as we finally have reasons for real flows moving from country to country as they start to consider normalisations of interest rates and other economic policies. Once one of the majors starts to normalise interest rates it will crystallise expectations on a few of the others and we will see further clarity in the signals between the asset classes as the normalisations progress. Granted, this make take the better part of a year to play out and it should be noted that China slowing down and Europe’s problems may put a damper on this. However, the pendulum swings and we believe the economic news in the pipeline will resume its uptrend and be good for growth and investment flows delivering clear signals that our strategy can exploit.

Our strategy relies on the movements in interest rates to determine the flows in the currency markets, not on the actual levels of rates between different countries and is thus not a carry trade. During long periods where interest rates are moving as the primary instrument of monetary policy, our strategy has shown itself to deliver consistent superior risk-adjusted returns. With the return of volatility, continuing growth from Canada, Britain and the US and rather different stories from the rest of the G10, we are already witnessing divergences in swaps rates and decent moves in the currencies out of ranges that were in place for the previous couple of years. The chart below features just three currency pairs (USDJPY, EURGBP & CADNOK) which have seen accelerated moves over the past 6 months.

(source: Bloomberg)

(source: Bloomberg)

Given these circumstance it is hard not to be excited about the prospects for our strategy over the coming months and years. The future may be an incomplete equation, but with the right tools and analysis, we believe we can stack the odds in our favour to maximise our investors’ chances for success.

source:BarclayHedge

source:BarclayHedge

For further information on Sequoia’s award-winning short-term systematic FX strategy please contact: investor.relations@sequoiacapfm.com

related articles:

Promising Results from Automated FX Trading Strategy using Country Sentiment Factors (Aug 2013)

FX Trading Signals From Systematic News Flow Analysis (Jan 2013)

One Response to “The Environment Is Good For Systematic FX As Well As CTAs”

Read below or add a comment...