By Simon Kerr, Publisher of Hedge Fund Insight

Changes to capital requirements imposed on banks by regulators are expected to have a significant impact on hedge fund-related activity. Indeed in only the last week or so two industry insiders told Hedge Fund Insight independently that it was THE biggest factor driving change in the hedge fund industry. As more capital has to be held by banks against financing to hedge funds from prime brokerage/prime finance so bank management has had a strategic decision to make – to maintain margins banks have to cut costs or raise fees. The senior management of the banks that provide finance to hedge funds have universally decided to raise fees to that client base. To a degree the margins of both provider and client are under pressure here.

Against this tough (and increasingly tough) commercial background it was interesting to hear some comments from a senior executive of Citigroup at the recent conference Morgan Stanley Financials Conference.

![]()

![]()

![]() Jamie Forese has not long been appointed President of Citigroup, and is the Chief Executive Officer of the Institutional Clients Group (ICG). At the Conference he was interviewed by Morgan Stanley analyst Betsy Graseck.

Jamie Forese has not long been appointed President of Citigroup, and is the Chief Executive Officer of the Institutional Clients Group (ICG). At the Conference he was interviewed by Morgan Stanley analyst Betsy Graseck.

Here are some extracts from the transcript, with highlighting by Hedge Fund Insight:

BETSY GRASECK: Can we talk a little bit about Citigroup’s capital position and how that can be an advantage for you? Obviously Citigroup has a very robust capital position and nice Statutory Liquidity Ratio (SLR). And so I would think that that would give you some advantage relative to peers in some of the businesses that you’re on.

JAMIE FORESE: Yeah. Well first of all, I’d say that overall, our strong capital position is an advantage to the bank overall and what it fundamentally means is that we have plenty of capital to support client needs. So as our clients require more capital, we’ve got it, and we will deploy it provided that we can meet threshold returns in our activities. And that’s not just an advantage to ICG; that’s an advantage to the consumer business as well. And to the extent we have – as you well know, the extent we feel we have excess capital, more than we can realistically deploy now and to the near future, we’d like to return that. We think that – we agree that that’s a big driver of shareholder value, is being able to accelerate our capital return program.

As it relates to ICG, given that the SLR is one of our least binding constraints in our own capital, it means that we can use SLR where we have good businesses on a risk-adjusted basis. We have good uses for capital on a risk-adjusted basis that may not be good uses on an SLR basis. We have the luxury of being able to do that. And so that does help in a few things that we are trying to develop: the prime finance business, the equity finance business overall, the set of delta one activities in equities. Those are good returns on risk-adjusted capital but not great returns on SLR. So, if SLR were our binding constraint, and it is for some firms, they are going to be pressuring those activities, whereas for us, because we have SLR capacity so to speak, we can deploy a little bit more balance sheet in the area and generate attractive returns on equity for shareholders.

BETSY GRASECK: Sure.

JAMIE FORESE: So it is, I think on a – there’s lots of challenges when you try to invest, but that is a little bit of an advantage for us, yes.

BETSY GRASECK: You were brought up equities, and I think recently, your European head of equities, Tim Gately, said that he thought the 1Q wasn’t just a blip for the industry and we should see strength continue, right? And I guess the question is, how are you thinking about your equities business? There’s been some volatility there, and I know that you guys have been working on driving to more consistent earnings, so you could explain what kind of is behind that thought process?

JAMIE FORESE: Equities is one of those businesses, when I was talking before about the review we did several years ago about our product spectrum, equities was one of those businesses that is – we’re amongst the very smallest of the global equity houses in terms of revenues. And we looked at it to see, is this something we should stay in, should we exit it, or what are we going to do about it? And we, again, consciously made the decision that we should invest in it, make it more efficient and make it more profitable. And we did that. That is core. Generating profitability is now a foundation of being able to grow it.

And while we’ve improved the equities business, we still have some things we are working on. One is, it’s still a little inconsistent from one quarter to the next. We can have some decent solid quarters, and then we seem to disappoint a little bit. We’re really trying to see what we can do to steady out the performance (in equities).

One of the things that is underlying that is to be stronger in prime finance and delta one products. The reported equities segment is made up of a number of things: the cash equities business, which is both high-touch, low-touch, or medium-touch execution business; there’s the traditional derivatives business; then you have the whole broad category of delta one businesses, then equity and prime finance.

That equity and prime finance business, the delta one category are more recurrent types of businesses. And so when you build a franchise there and you have revenue in one quarter, you’re more likely to generate it again the second quarter. Yes, there’s some volatility too, but it’s not as volatile as traditional derivatives for the cash business. And so, one of the things that we’re looking at doing now that we’ve got into levels of profitability that we do think are extremely competitive now compared to the industry overall is to look where we can invest in the business, and particularly in things like equities to try to build that franchise up. And again, we have realistic goals there. We are not going to set a silly, unrealistic goal of trying to be in the top three in 12 months’ time. That’s not credible. But we do think that we can move from our current position just gradually up with some solid, steady investment in the business.

.

.

.

BETSY GRASECK: Okay. All right. And then just lastly on the ROTCE (Return on Tangible Capital Employed), you mentioned that’s really a critical driver of how you think about the business and your success in running it. You’ve got 13% return on tangible capital if we calculated it correctly, and you are contributing 60% to Citicorp’s earnings. So a big number in both ways. I guess I’m just wondering, do you feel like there is room to move up that 13% or is that the kind of steady state and you’ve gotten it already to that very high best-in-class ratio?

JAMIE FORESE: Well, again, so there’s three principal levers to improve the return.

On the revenue side, find a way to make them go higher; the expense side, find a way to make them go lower or deploy less capital in the denominator. I think on the expense side, when you look at our operating efficiency and if we stay on course to hit our target for 2015, that is going to be an extremely competitive, if not industry- leading operating efficiency for the segment amongst our peers. And there’s only – there’s a limitation to just how competitive you can be with your operating efficiency because improvements in operating efficiency tend to come only because you’re not investing enough in the future or you may not be paying your people competitively enough too, which has the long-term effect of hollowing out your talent. So those aren’t ways in which we want to improve the efficiency ratio further.

So having done a good job I think over the last few years on expenses, we’re not done in finding productivity enhancements and gains, but it is coming to an end. The story is not going to be as good going forward.

So, we need to grow the revenue line to improve, which we think, if we can get a higher-rate environment, and we’ve – John and others, Mike, have spoken publicly about the benefit that that has to the bank in a higher-rate environment and I think it’s somewhat reflected in today’s – the moves in bank pricing today as we start to anticipate higher rates. So that will be a boost as well, and I think that’s largely a pretty efficient boost to the bottom line too, because we don’t necessarily have a lot of expenses that correspond to that increase. So, and again, we’re still very focused on growing share of wallet in our segment too. So that hasn’t come to an end, and even though it may be easier in some product areas to grow wallet share than in others where we are more saturated, that’s still a focus of the bank.

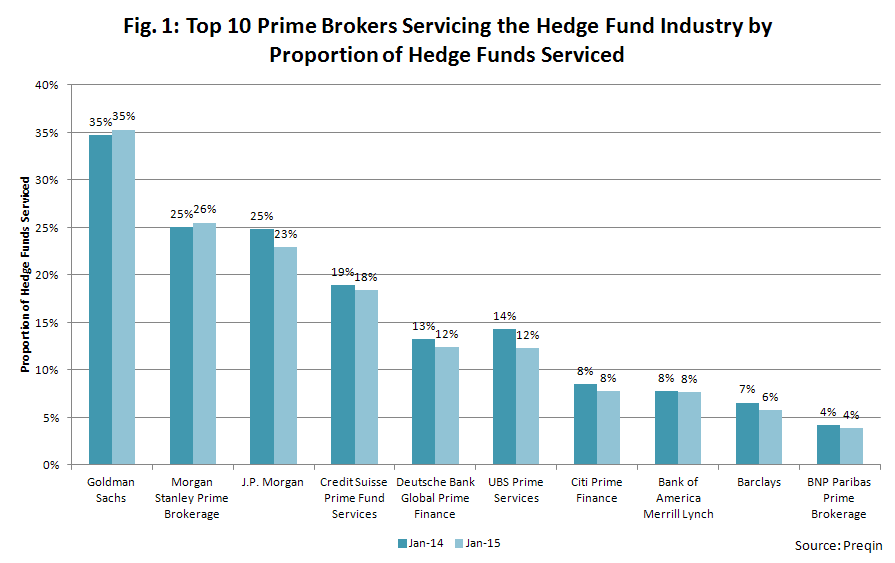

Citigroup has some way to go to get into the very top bracket of prime brokers. As figure 1 shows they rank 7th in the industry by percentage of funds served, but even if they doubled their share in the medium term they would still be 5th ranked in size.

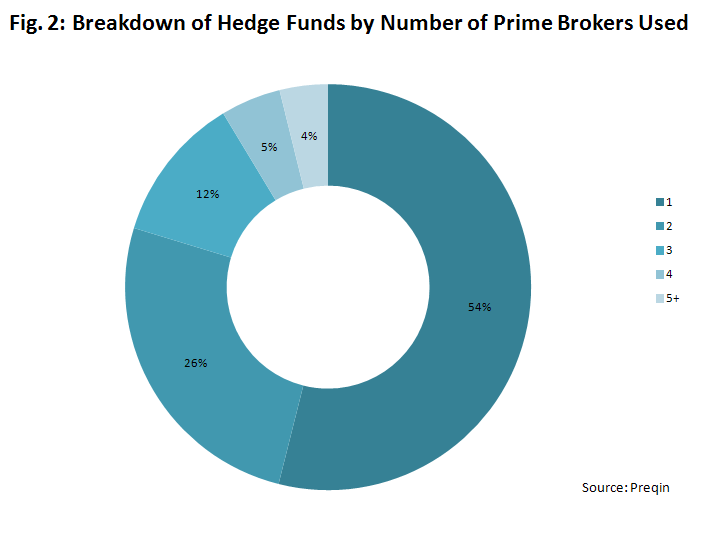

If that makes the strategic goal of growing the prime finance business of Citigroup seem too difficult to achieve, even if the bank’s most senior executives back it with the bank’s balance sheet, then reflect on Figure 2.

Post-Credit Crunch all hedge fund management groups of commercially significant size use more than one PB – so the 54% of hedge funds using one prime broker in the graphic above are the 6,000 hedge funds with small assets under management. The opportunity Citi are looking to take is to expand their share of existing PB client business – going from number 4 to number 3, and 3 to 2 etcetera of the ranking with each client. In an era when most PBs are finding it increasingly difficult to bring their balance sheet to bear in prime brokerage because of capital requirements at the holding company level Citigroup does have a shot at meaningfully changing its ranking in prime brokerage if their B/S is made available there.

Related articles:

Citi To Exit Hedge Fund Administration (Jan 2015)

Big Changes For Hedge Funds In Management Of Counterparties & Collateral Seen By Citi (July 2014)

Margin Pressures Evident In Citi Hedge Fund Survey (Dec 2013)