From Eurekahedge

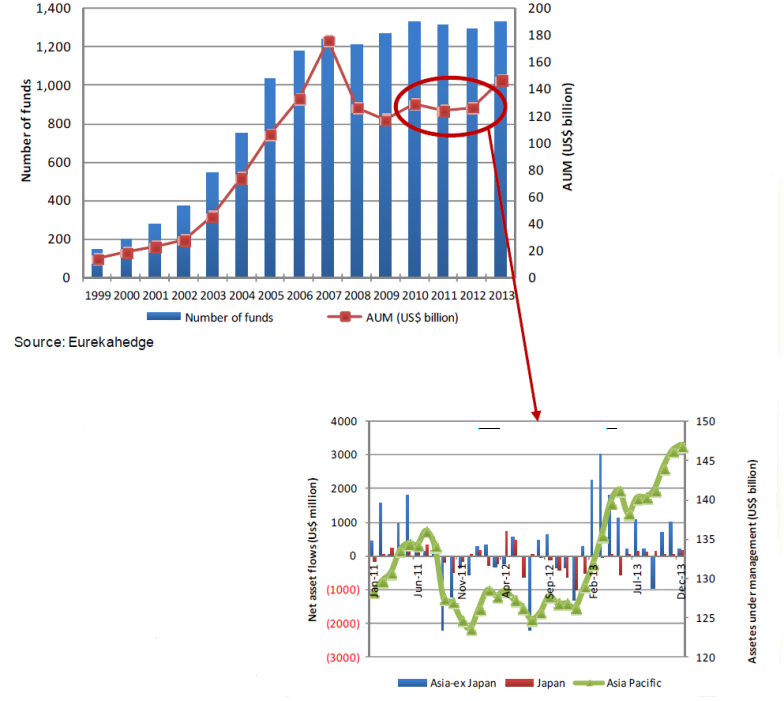

The Asian hedge fund industry  delivered excellent performance in 2013, beating underlying markets and outperforming its global peers during the year. The Eurekahedge Asia Hedge Fund Index gained 16.10% in 2013 with the total assets under management (AUM) increasing by US$20.6 billion. This brings the total size of the Asian hedge fund industry to US$147.0 billion managed by a population of 1,333 hedge funds.

delivered excellent performance in 2013, beating underlying markets and outperforming its global peers during the year. The Eurekahedge Asia Hedge Fund Index gained 16.10% in 2013 with the total assets under management (AUM) increasing by US$20.6 billion. This brings the total size of the Asian hedge fund industry to US$147.0 billion managed by a population of 1,333 hedge funds.

The size of the industry stood at US$14 billion as at end-1999, and over the next eight years it grew to US$176 billion by end-2007 – a period which saw a strong growth in the hedge fund industry’s tilt towards Asia. As at end-2007, the total fund population in the region stood at 1,237 funds up from 145 funds in 1999. Gains realised over this period were partially reversed by the advent of the global financial crisis which saw the Eurekahedge Asia Hedge Fund Index decline by 20.31% in 2008, ushering in a spate of fund liquidations as managers struggled to deal with negative returns and redemption requests from investors. The industry bottomed out in April 2009 with AUM declining to a low of US$104.8 billion before witnessing a rebound of sorts amid rallying equity markets and some positive asset flows in the second half of 2009. The industry continued its upward trajectory in 2010, realising strong performance-based growth as the Eurekahedge Asian Hedge Fund Index gained 9.07% during the year.

Figure 1: Industry growth since 1999

Note: All figures are in US$ billion, and rounded up to 1 decimal place, Source: Eurekahedge

Note: All figures are in US$ billion, and rounded up to 1 decimal place, Source: Eurekahedge

Figures 2a and 2b track the pace of launches and closures in the Asian hedge fund space since 2008. Hedge fund attrition rates spiked up post-the financial crisis with a total of 184 fund liquidations in 2008. The number of fund closures dwarfed launches in the fourth quarter of 2008 as fund managers posted heavy losses amid a global financial meltdown following the collapse of Lehman Brothers. The industry saw some respite from mid-2009 to end-2010 as launch activity picked up while fund liquidation was relatively subdued. This period saw a number of fund managers set up shop in Asia, in particular Hong Kong and Singapore, as financial regulation in the US clamped down on investment banks’ proprietary desks. The second half of 2011 saw another spike in fund liquidations amid the worsening global economic outlook – with Asia ex-Japan and globally focused funds seeing the highest attrition rates. Liquidation rates remained high throughout 2012, taking their toll on the smaller hedge funds which failed to qualify for their performance fees.

Asset allocation by geographic mandate in Asia has been influenced by an overall decline in AUM in the region and a general rebalancing of manager portfolios to gain wider exposure to the underlying markets. This trend has driven an increase in the AUM of globally mandated funds which have seen their share increase from 14.8% in 2007 to 23.6% by 2013. Asset allocations to single country mandated funds, such as those focused on Japan, India, Korea and Taiwan have also collectively decreased from 17.5% in 2007 to 14.0% by 2013 as managers have sought to diversify their regional exposure. The share of emerging markets focused funds has also dropped by 2.9% since 2007 as investors have sought exposure to the underlying markets via globally mandated funds. As emerging markets come under further pressure on the back of the wind-down in the Fed’s QE, this trend is likely to gain more momentum. Managers investing in Greater China have seen their share of AUM increase by 6.3% since 2007 as fund managers are attracted by the growth in high net worth individuals (HNWI) numbers in the region. Greater China focused hedge funds delivered an impressive 18.88% in 2013 comfortably outperforming underlying markets.

Asian industry breakdown by strategy

In terms of the composition of the industry by strategic mandate, the Asian hedge fund industry delineates some interesting trends – the most striking being a 14.9% decline in the share of long/short equities funds since 2007. A great part of this contraction happened during the financial crisis; the Eurekahedge Asia Long Short Equities Hedge Fund Index declined 21.6% in 2008 as long/short equities managers posted heavy losses. Furthermore, as the Asian hedge fund industry has matured, managers have diversified away from long/short equities strategies (which are strongly correlated to the underlying markets) towards event driven, multi-strategy, relative value and fixed income strategies which have seen their share of AUM increase by 8.6%, 6.8% and 3.1% respectively since 2007. We expect this diversification to increase in the region, especially for Greater China focused funds as the Chinese economy transitions to relatively lower rates of economic growth which will squeeze gains derived from a largely beta driven approach.

Figures 6a-6c: Breakdown by strategy (by assets under management)

Head office location

Figures 7a and 7b display the changes in head office location of Asian hedge funds over the years. In 2007, 37.5% of the funds were based either in the US or UK, which has declined to a share of 27.7% by 2013 as Asia has seen strong launch activity centred on its key financial centres. Hong Kong is now the premier choice of location for Asian hedge funds, increasing from a market share of 15.8% in 2007 to 20.9% by 2013. A similar shift has been seen in favour of Singapore which now hosts the second largest population of Asian hedge funds; 15.4% by market share. Australia’s share has declined marginally although it still ranks in the top five locations of choice for fund managers in Asia.

The above trends have been driven by a combination of factors that have pushed investors away from the more developed hedge fund markets in the West towards the high growth economies in the East. Regulatory pressures and relatively higher taxation rates in Europe and the US, coupled with an increasingly competitive hedge fund landscape have made it difficult for fund managers to trade profitably. Asian markets on the other hand are growing and less crowded, hence offering ample opportunities for managers. The exponential rise in the number of accredited investors (HNWI) in Asia promises fund managers with a pool of potential investors and thus the prospects of locating in Asia have appeared even more attractive. Local factors, such as the presence of seasoned traders who have built their expertise through years of experience in the financial markets, have further contributed to the gravitation towards Asia.

Figures 7a-7b: Head office locations by number of funds

Eurekahedge is the world’s largest independent data provider and research house dedicated to the collation and development of alternative investment data. Eurekahedge was launched in 2001, and since then has aggressively grown its research data banks from 162 funds to over 29,000 alternative funds globally. Eurekahedge’s comprehensive databases feature up-to-date indices, detailed fund profiles, performance measurements and rankings of funds, providing solutions and insights into the individual funds or entire portfolios as well as evolving asset classes and markets. For further information go to www.eurekahedge.com