By Thomson Reuters/Hedge Fund Insight staff

Completed Distressed Debt and Bankruptcy Restructuring activity totaled US$59.9 billion during the first half of 2015, a 44% decrease from the first half of 2014. The number of completed deals also saw a significant decrease, with 109 deals during the first half of 2015 compared to the 165 during the same period last year. The two largest completed transactions during the first half of 2015 were the US$14.6 billion debt restructuring of Dubai World and the US$6 billion debt restructuring of ITR Concession Co LLC.

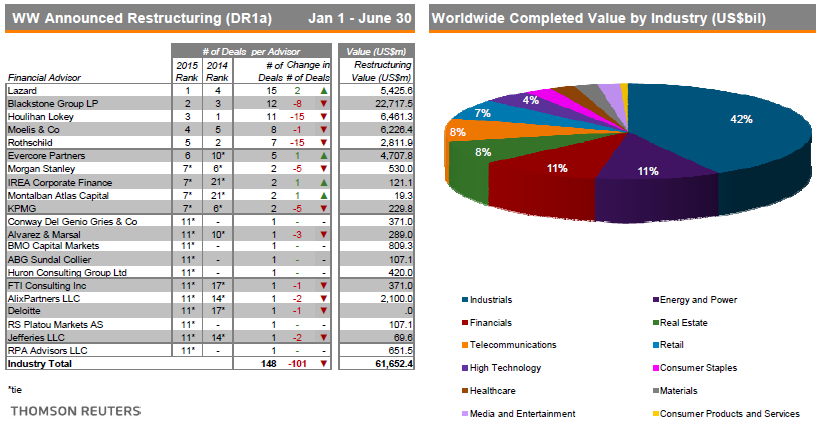

US completed deal activity totaled US$18.3 billion during the first half of 2015, a 34% decrease compared to the first half of 2014. There were 37 restructuring transactions completed in the US during the first half of the year, 14 fewer deals than the same period last year. The Industrials sector accounted for 40% of the US debt restructuring market, followed by Telecommunications, with a 27% share.

EMEA completed distressed debt restructuring deal volume totaled US$37.1 billion during the first half of 2015, marking a 46% descrease in activity compared to the first half of 2014. Industrials led all sectors in EMEA, with 50% of total completed EMEA distressed debt restructuring deal volume.

Asia Pacific (including Japan) completed deal volumes during the first half of 2015 reached US$2.7 billion from 26 deals, down 64% from the same period last year. High Tecnhology was the most active sector, capturing 67% of the

market, followed by Industrials and Energy & Power, accounting for 22% and 11% of the market, respectively.

Distressed investing is a pipeline business. Ideally investors in distressed prefer to buy the securities at large discounts – those levels of discounts are more frequent when economic conditions have been deteriorating for some time. That causes companies to be in distress across the whole economy, and makes the most indebted companies particularly vulnerable – large discounts occur because there is a lot of merchandise to choose from.

Coming out of the pipeline, distressed investors want to recapitalize the companies/equitize their debt and are best served by a buoyant economic and stockmarket background when that occurs. Stockmarkets are still near post-Credit Crunch highs, and economic growth has rumbled on for most of the last 4-5 years. In short this has been a good environment for realizations.

The Thomson Reuters data for the first half of 2015 shows that there are fewer deals to choose from for distressed managers to pump into their own pipelines (portfolios). However the environment for realizations remains good, but that has not come through to the returns of distressed managers. The table below shows that after very good returns in 2012 and 2013, the returns from distressed funds at the index level were a minor negative last year. The 2014 returns included five negative monthly returns in the second half of the year.

In contrast, the first six months of 2015 have included four positive monthly returns, and YTD distressed funds have been up to a small degree (0.64%). Whilst not tearing it up, the returns of distressed funds are better, taking the index returns as a diffusion index/indicator. Investors in distressed securities funds have been equivocal – after committing fresh capital to the strategy in the last couple of years, investors have kept their capital in this year, but not added to it.

In the second of 2015 investing institutions will be looking to add to their exposures to distressed investing, waiting for evidence to show itself that the Oaktree Indicator* has led returns with only a short lag (one or two quarters).

*For more on the Oaktree Indicator see: Oaktree Capital Indicator For Distressed Investing Turns Positive